Commentary

Small Cap Equity 1Q 2024

ARISTOTLE CAPITAL BOSTON, LLC

Markets Review

Small caps added to their fourth quarter 2023 gains to begin the year with the Russell 2000 delivering a total return of 5.18%. Resilient economic data helped support investor sentiment during the first quarter. The U.S. economy was confirmed to have grown by more than expected during Q4 2023, while survey data from the composite Manufacturing Purchasing Managers’ Index (PMI) reentered expansionary territory. Stickier inflation prints and healthy labor data, however, are among the factors that have altered expectations about the timing and magnitude of interest rate cuts over the past few months. Earlier this year, the federal funds futures market had priced in as many as six 25-basis-point cuts to the federal funds target rate for this calendar year. Now that number is down to three, with some market prognosticators suggesting that the Fed won’t lower interest rates this year at all, due to the strength of the economy and the risk that inflation will remain too high.

Stylistically, growth stocks outperformed their value counterparts during the quarter as evidenced by the Russell 2000 Growth Index returning 7.58% compared to 2.90% for the Russell 2000 Value Index. Growth’s outperformance was buoyed by outsized gains from two information technology sector companies – Super Micro and MicroStrategy. Within the Russell 2000 Index, Super Micro Computer represented the largest single-stock weight ever at quarter end. Together, Super Micro and MicroStrategy accounted for over 37% of the Russell 2000’s quarterly gain on a contribution to return basis. The concentration conundrum has been well documented within the U.S. large cap indices but rarely influences the more diversified Russell 2000 Index to this degree. These issues should abate following the June reconstitution of the Russell indices, however, small cap active managers will miss out on any immediate benefit from a retracement of these gains as these two companies are poised to graduate into the larger cap Russell 1000 index.

At the sector level, seven of the eleven sectors in the Russell 2000 Index recorded positive returns during the first quarter, led by strong returns in the Information Technology (+12.82%), Energy (+11.86%) and Industrials (+8.80%) sectors. Conversely, Communication Services (-4.94%), Utilities (-3.59%), and Real Estate (-1.52%) all underperformed and posted negative returns. Looking at market factors, Momentum, Growth, and High Short Interest outperformed while Value, Low Beta, and Negative Earners underperformed.

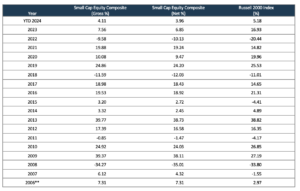

Sources: CAPS Composite Hub, Russell Investments

Past performance is not indicative of future results. Returns are presented gross and net of investment advisory fees and include the reinvestment of all income. Gross returns will be reduced by fees and other expenses that may be incurred in the management of the account. Net returns are presented net of actual investment advisory fees and after the deduction of all trading expenses. Aristotle Small Cap Equity Composite returns are preliminary pending final account reconciliation. Please see important disclosures at the end of this document.

Performance Review

For the first quarter of 2024, the Aristotle Small Cap Equity Composite posted a total return of 3.96% net of fees (4.11% gross of fees), trailing the 5.18% total return of the Russell 2000 Index. Underperformance was driven by security selection while allocation effects positively contributed. Overall, security selection was weakest within the Information Technology, Health Care, and Consumer Staples sectors and strongest in Consumer Discretionary, Materials, and Energy. From an allocation perspective, the portfolio benefitted from overweight in Industrials and an underweight in Financials, however, this was partially offset by underweights in Energy and Consumer Discretionary.

| Relative Contributors | Relative Detractors |

|---|---|

| The AZEK Company | ModivCare |

| Itron | QuidelOrtho |

| Dycom Industries | Huron Consulting Group |

| AerCap | Mercury Systems |

| Ardmore Shipping | Matthews International |

CONTRIBUTORS

The AZEK Company (AZEK), a leading manufacturer of residential building products, primarily focused on wood-alternative decking, railing and trim, benefited from strong fundamental performance revealed in the company’s latest earnings release after the company reported favorable broader business trends, expanding margins, and strong sales. We maintain our position, as we believe the strong secular demand backdrop for alternative, sustainably sourced building products along with company-specific margin improvements should benefit shareholders in periods to come.

Itron (ITRI), a global manufacturer and distributor of electric, water and gas meters and advanced meter systems, benefitted from continued momentum in the operational outlook for its business, a growing backlog of higher margin business, and an easing of supply chain conditions. We maintain a position, as we believe the company remains well-positioned to benefit from power grid modernization efforts, which should continue to drive demand for the company’s smart metering and grid monitoring solutions. Additionally, we believe an acceleration in the company’s services and SaaS-based revenue will improve the earnings and margin profile of the business moving forward.

DETRACTORS

ModivCare (MODV), a Colorado-based healthcare services company that provides non-emergency medical transportation (NEMT), homecare services, and remote monitoring to Medicaid and Medicare populations declined during the period amid working capital challenges and a slower than expected start to the year. We continue to maintain a position despite near-term challenges as we believe the longer-term fundamental outlook for the business remains attractive and that an upcoming monetization event should alleviate investor concerns regarding the company’s credit profile.

QuidelOrtho (QDEL), a developer and manufacturer of point-of-care and near-patient diagnostic solutions declined during the period after delivering results that were below investor expectations. We maintain our position, as we believe the company’s recent efforts to broaden its product portfolio and diversify the business away from respiratory illness should result in less volatile operating results and create additional value for shareholders.

Recent Portfolio Activity

| Buys/Acquisitions | Sells/Liquidations |

|---|---|

| PowerSchool | ATN International |

| Capital Product Partners | |

| SP Plus |

BUYS/ACQUISITIONS

PowerSchool (PWSC), a leading provider of cloud-based software for K-12 education in North America, was added to the portfolio. Overall, we believe the company stands to benefit from the growing demand for digital education solutions, an increased need for efficiency in school operations, and a favorable funding environment. Moreover, we believe the company’s ability to innovate and adapt to the evolving needs of the education sector while expanding its capabilities and solutions should result in up-sell opportunities that can further create value for their customers and shareholders.

SELLS/LIQUIDATIONS

ATN International (ATNI), a provider of telecommunications services to rural, niche, and other under-served markets, was removed from the portfolio. Despite the company’s efforts to expand its broadband network in recent years, a variety of factors contributed to our decision to step away from our investment including competitive pressures and our general concerns regarding the company’s capital allocation strategy moving forward.

Capital Product Partners (CPLP), a marine shipping company that operates LNG carriers and containerships, was removed from the portfolio during the quarter after a period of strong share price performance given our view that the future risk/reward potential of the company had narrowed.

SP Plus (SP), a provider of parking management, payment services, facility maintenance and event logistics solutions, was removed from the portfolio after being acquired by Metropolis Technologies.

Outlook

We continue to remain optimistic about the long-term potential for the small-cap segment of the U.S. market, although we readily admit that making short-term calls about the future direction of the market following a strong run (+30% since the Russell 2000 October 2023 low) is a challenging and dubious task. As we look out to the remainder of 2024, while we are encouraged by the continuing signs of economic stability, we recognize that calls for a soft landing are now consensus, sentiment may be overly optimistic, and markets seem priced for very little risk. So, despite greater clarity over the Fed’s path from here, there still remains a long list of items creating uncertainty that could lead to greater volatility in 2024 including, but not limited to, signs that inflationary pressures have not yet dissipated, geopolitical tensions, U.S. equity index concentration issues, ongoing commercial real estate concerns, and the looming presidential election. We are well aware that most of these issues are well known, but the timing and magnitude of the impact of any and all of these issues remains unpredictable. Therefore, as we always have, we will continue to avoid the temptation to forecast their outcome in favor of assessing the potential impact from a range of potential outcomes within our company‐specific, bottom-up analysis, and quality focus.

From an asset class perspective, valuations of small versus large continue to remain near multi-decade lows, which we believe suggests a more favorable setup for small caps relative to large caps in the periods to come (16.0x P/E for the Russell 2000 Index vs. 21.8x P/E for the Russell 1000 Index). Additionally, earnings growth is expected to improve for small caps in 2024 and outpace that of large caps, which we believe provides further fundamental support and potential upside for the asset class. Against a backdrop of moderating inflation, normalized interest rates, and a still growing U.S. economy, it looks to us that small-cap’s lengthy stretch of relative underperformance may be long in the tooth. If the economy continues to stabilize, our view is that valuations are likely to rise for those businesses that have largely sat out the mega-cap performance regime. It also helps that the well-noted concentration in large caps is reaching 50-year highs and small cap valuation relative to large cap is at multi-decade lows, therefore any fundamentally driven repositioning is likely to benefit small caps more than larger companies, in our view. Lastly, we believe smaller caps remain better positioned to benefit from the reshoring of U.S. manufacturing, the CHIPS Act, and several infrastructure projects on the horizon.

Positioning

Our current positioning is a function of our bottom-up security selection process and our ability to identify what we view as attractive investment candidates, regardless of economic sector definitions. Overweights in Industrials and Information Technology are mostly a function of our underlying company specific views rather than any top-down predictions for each sector. Conversely, we continue to be underweight in Consumer Discretionary, as we have been unable to identify what we consider to be compelling long-term opportunities that fit our discipline given the rising risk profiles of many retail businesses and a potential deceleration in goods spending following a period of strength. While the portfolio’s allocation to Health Care is modestly below that of the benchmark, we continue to remain underweight the Biotechnology industry as many companies within that group do not fit our discipline due to their elevated levels of binary risk. Given our focus on long-term business fundamentals, patient investment approach and low portfolio turnover, the strategy’s sector positioning generally does not change significantly from quarter to quarter. However, we may take advantage of periods of volatility by adding selectively to certain companies when appropriate.

The opinions expressed herein are those of Aristotle Capital Boston, LLC (Aristotle Boston) and are subject to change without notice.

Past performance is not indicative of future results. The information provided in this report should not be considered financial advice or a recommendation to purchase or sell any particular security. There is no assurance that any securities discussed herein will remain in an account’s portfolio at the time you receive this report or that securities sold have not been repurchased. The securities discussed may not represent an account’s entire portfolio and, in the aggregate, may represent only a small percentage of an account’s portfolio holdings. The performance attribution presented is of a representative account from Aristotle Boston’s Small Cap Equity Composite. The representative account is a discretionary client account which was chosen to most closely reflect the investment style of the strategy. The criteria used for representative account selection is based on the account’s period of time under management and its similarity of holdings in relation to the strategy. It should not be assumed that any of the securities transactions, holdings or sectors discussed were or will be profitable, or that the investment recommendations or decisions Aristotle Boston makes in the future will be profitable or equal the performance of the securities discussed herein. Aristotle Boston reserves the right to modify its current investment strategies and techniques based on changing market dynamics or client needs. Recommendations made in the last 12 months are available upon request.

Returns are presented gross and net of investment advisory fees and include the reinvestment of all income. Gross returns will be reduced by fees and other expenses that may be incurred in the management of the account. Net returns are presented net of actual investment advisory fees and after the deduction of all trading expenses.

Effective January 1, 2022, the Aristotle Small Cap Equity Composite has been redefined to exclude accounts with meaningful industry-specific restrictions or substantial values-based screens hampering implementation of the small cap strategy.

Effective January 1, 2022, the Russell 2000 Value Index was removed as the secondary benchmark for the Aristotle Capital Boston Small Cap Equity strategy.

All investments carry a certain degree of risk, including the possible loss of principal. Investments are also subject to political, market, currency and regulatory risks or economic developments. International investments involve special risks that may in particular cause a loss in principal, including currency fluctuation, lower liquidity, different accounting methods and economic and political systems, and higher transaction costs.

These risks typically are greater in emerging markets. Securities of small‐ and medium‐sized companies tend to have a shorter history of operations, be more volatile and less liquid. Value stocks can perform differently from the market as a whole and other types of stocks. The material is provided for informational and/or educational purposes only and is not intended to be and should not be construed as investment, legal or tax advice and/or a legal opinion. Investors should consult their financial and tax adviser before making investments.

The opinions referenced are as of the date of publication, may be modified due to changes in the market or economic conditions, and may not necessarily come to pass.

The firm’s coverage of Signature Bank includes time at a predecessor firm.

Aristotle Capital Boston, LLC is an independent investment adviser registered under the Investment Advisers Act of 1940, as amended. Registration does not imply a certain level of skill or training. More information about Aristotle Boston, including our investment strategies, fees and objectives, can be found in our Form ADV Part 2, which is available upon request. ACB-2404-26

Sources: CAPS Composite Hub, Russell Investments

Composite returns for periods ended March 31, 2024, are preliminary pending final account reconciliation.

*The Aristotle Small Cap Equity Composite has an inception date of November 1, 2006 at a predecessor firm. During this time, Jack McPherson and Dave Adams had primary responsibility for managing the strategy. Performance starting January 1, 2015 was achieved at Aristotle Boston.

**For the period November 2006 through December 2006.

Past performance is not indicative of future results. Performance results for periods greater than one year have been annualized.

Effective January 1, 2022, the Aristotle Small Cap Equity Composite has been redefined to exclude accounts with meaningful industry-specific restrictions or substantial values-based screens hampering implementation of the small cap strategy.

Effective January 1, 2022, the Russell 2000 Value was removed as the secondary benchmark for the Aristotle Capital Boston Small Cap Equity strategy.

Returns are presented gross and net of investment advisory fees and include the reinvestment of all income. Gross returns will be reduced by fees and other expenses that may be incurred in the management of the account. Net returns are presented net of actual investment advisory fees and after the deduction of all trading expenses. Please see important disclosures enclosed within this document.

The Russell 2000® Index measures the performance of the small cap segment of the U.S. equity universe. The Russell 2000 Index is a subset of the Russell 3000® Index representing approximately 10% of the total market capitalization of that index. It includes approximately 2000 of the smallest securities based on a combination of their market cap and current index membership. The Russell 2000 Growth® Index measures the performance of the small cap companies located in the United States that also exhibit a growth probability. The Russell 2000 Value® Index measures the performance of the small cap companies located in the United States that also exhibit a value probability. The Russell 1000® Index measures the performance of the large cap segment of the U.S. equity universe. The Russell 1000 Index is a subset of the Russell 3000® Index, representing approximately 90% of the total market capitalization of that index. It includes approximately 1,000 of the largest securities based on a combination of their market capitalization and current index membership. The volatility (beta) of the composite may be greater or less than the benchmarks. It is not possible to invest directly in these indices.