Markets Review

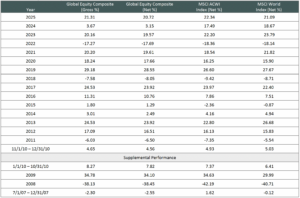

Sources: CAPS CompositeHubTM, Bloomberg

Past performance is not indicative of future results. Aristotle Value Equity WM Composite returns are presented pure gross and net of the maximum wrap fee and include the reinvestment of all income. Pure gross returns do not reflect the deduction of any trading costs or other fees and are supplemental to the net returns. Net returns are calculated by subtracting the highest applicable wrap/SMA fee, which includes trading costs and custodial fees, from the pure gross composite return. (From inception to 12/31/2015, the highest applicable wrap/SMA fee is 3.00% on an annual basis, or 0.75% quarterly. From 1/1/2016 to 12/31/2023, the highest applicable wrap/SMA fee is 2.00% on an annual basis, or 0.50% quarterly and 0.17% monthly from 1/1/2024 to present.) Aristotle Capital Composite returns are preliminary pending final account reconciliation. Please see important disclosures at the end of this document.

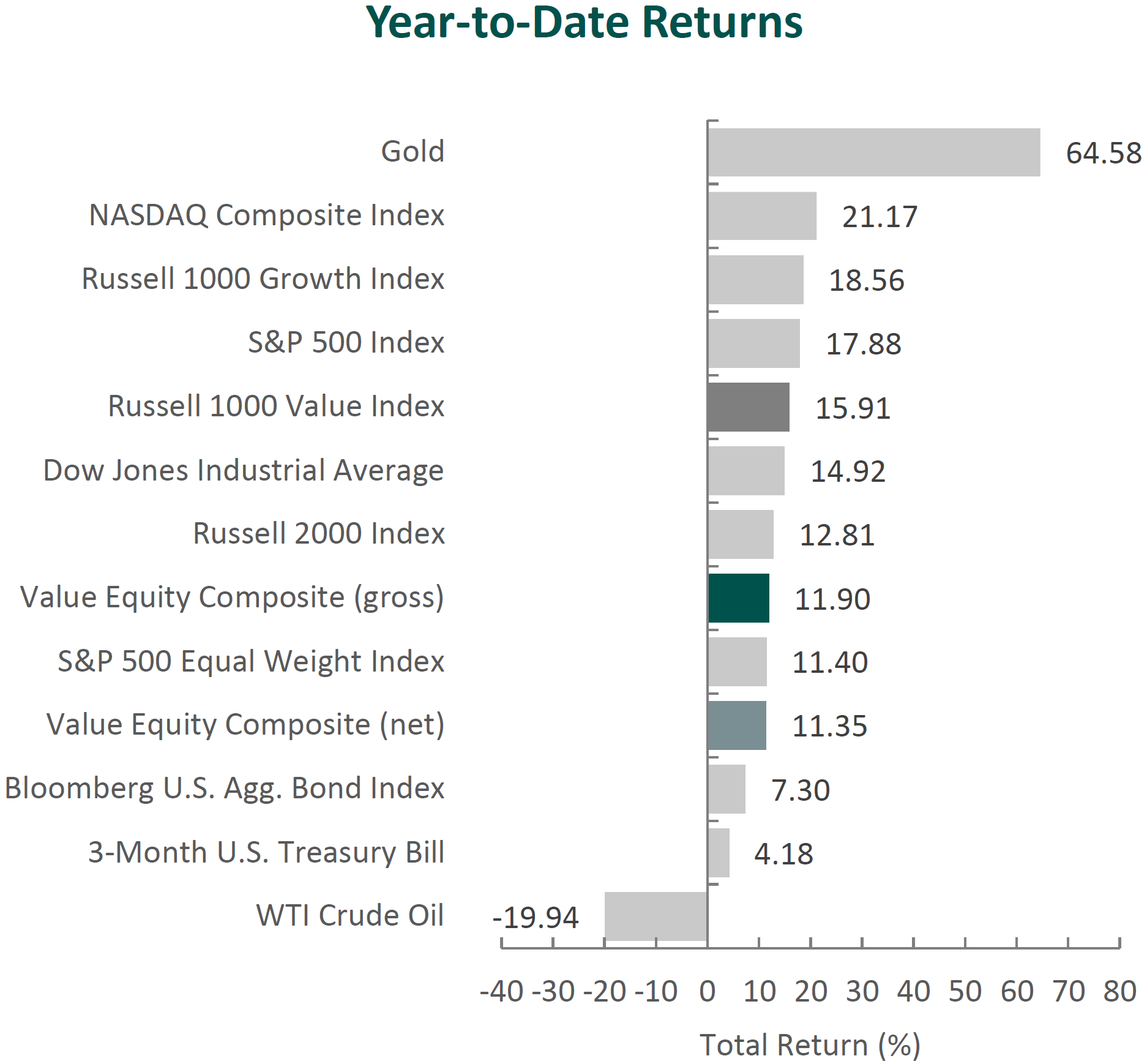

U.S. equity markets reached new all-time highs in the fourth quarter of 2025. The S&P 500 Index rose 2.66%, while fixed income markets also finished higher, with the Bloomberg U.S. Aggregate Bond Index up 1.10% for the quarter. Value stocks handily outperformed growth stocks—the Russell 1000 Value Index outperformed its Growth counterpart by 2.69%. Within the Russell 1000 Value Index, eight out of the eleven sectors posted positive returns. The best-performing sectors were Information Technology, Communication Services and Health Care, whereas Real Estate, Utilities and Consumer Discretionary were the weakest segments.

The U.S. economy continued to demonstrate resilience. Data released during the period showed that real GDP surged at a 4.3% annualized rate in the third quarter—the fastest quarterly growth in two years—driven primarily by robust consumer spending, with additional contributions from rising exports and increased government outlays. Despite this strength, consumer confidence deteriorated toward year-end; economists projected a moderation in spending, and concerns about the labor market persisted. The unemployment rate ticked up to 4.6% in November (a four-year high), though this level remains low by historical standards and is still consistent with an economy operating near full employment. Meanwhile, inflation moderated—the Consumer Price Index was up just 2.7% year-over-year in November, reaching its lowest level since July. Economists cautioned that recent unemployment and inflation figures were likely skewed by technical factors related to the 43-day government shutdown, which disrupted data reporting. This shutdown—the longest in U.S. history—forced approximately 1.4 million federal employees to go without pay and even led to temporary layoffs at some agencies before Congress passed a continuing resolution to reopen on November 12.

Given the mixed economic signals and uncertainty around the data, the Federal Reserve took a cautious stance. The Fed implemented two 0.25% interest rate cuts during the quarter, lowering the federal funds target range to 3.50%-3.75%. Fed Chair Powell emphasized a data-dependent approach, acknowledging risks to both sides of the Fed’s dual mandate. He noted the need to carefully assess incoming information, highlighting that policy would remain cautious and measured going into 2026.

Trade relations between the U.S. and China remained a key focus for markets. Early in the fourth quarter, tensions flared with tariff escalations and export controls. (China had dramatically expanded export controls on rare earth minerals, and the U.S. threatened 100% tariffs in retaliation.) Ultimately, President Trump and President Xi met at the Asia-Pacific Economic Cooperation (APEC) summit in South Korea and reached a one-year trade truce.

Corporate earnings remained robust. S&P 500 companies reported earnings growth of 13.6%, marking the fourth consecutive quarter of double-digit expansion. Of the 11 sectors within the S&P 500 Index, Information Technology recorded the strongest earnings growth of 29%. Artificial intelligence continued to be a major theme—more than 300 S&P 500 companies mentioned “AI” on their earnings calls during the fall. This enthusiasm helped propel mega-cap tech stocks higher and drive the market’s gains. However, as the quarter progressed, scrutiny increased around AI-related revenue circularity (companies buying AI services from each other to boost sales), the massive scale of AI-related capital spending, and the durability of longer-term returns on investment.

Annual Markets Review

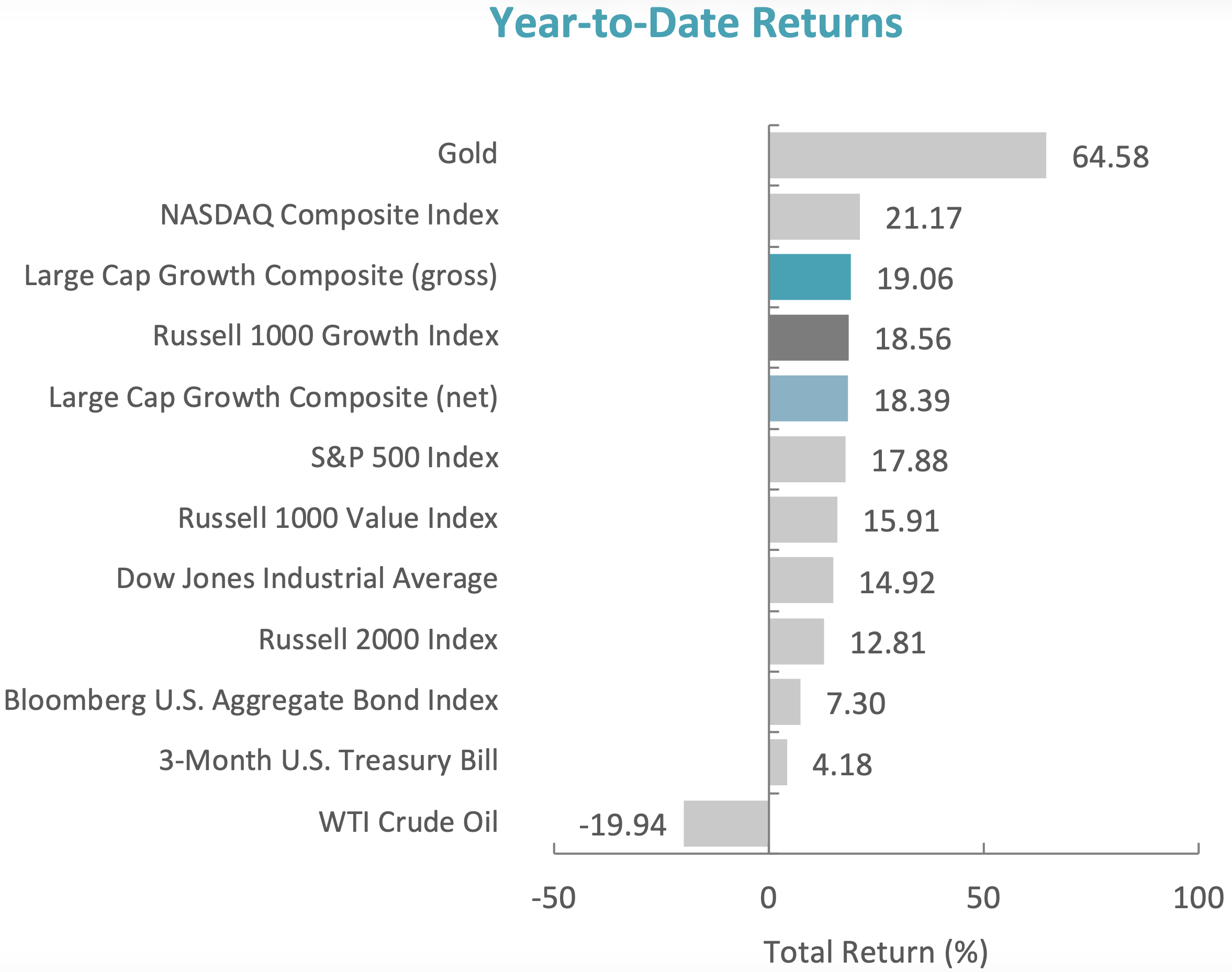

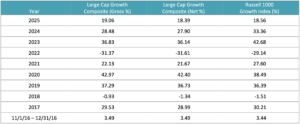

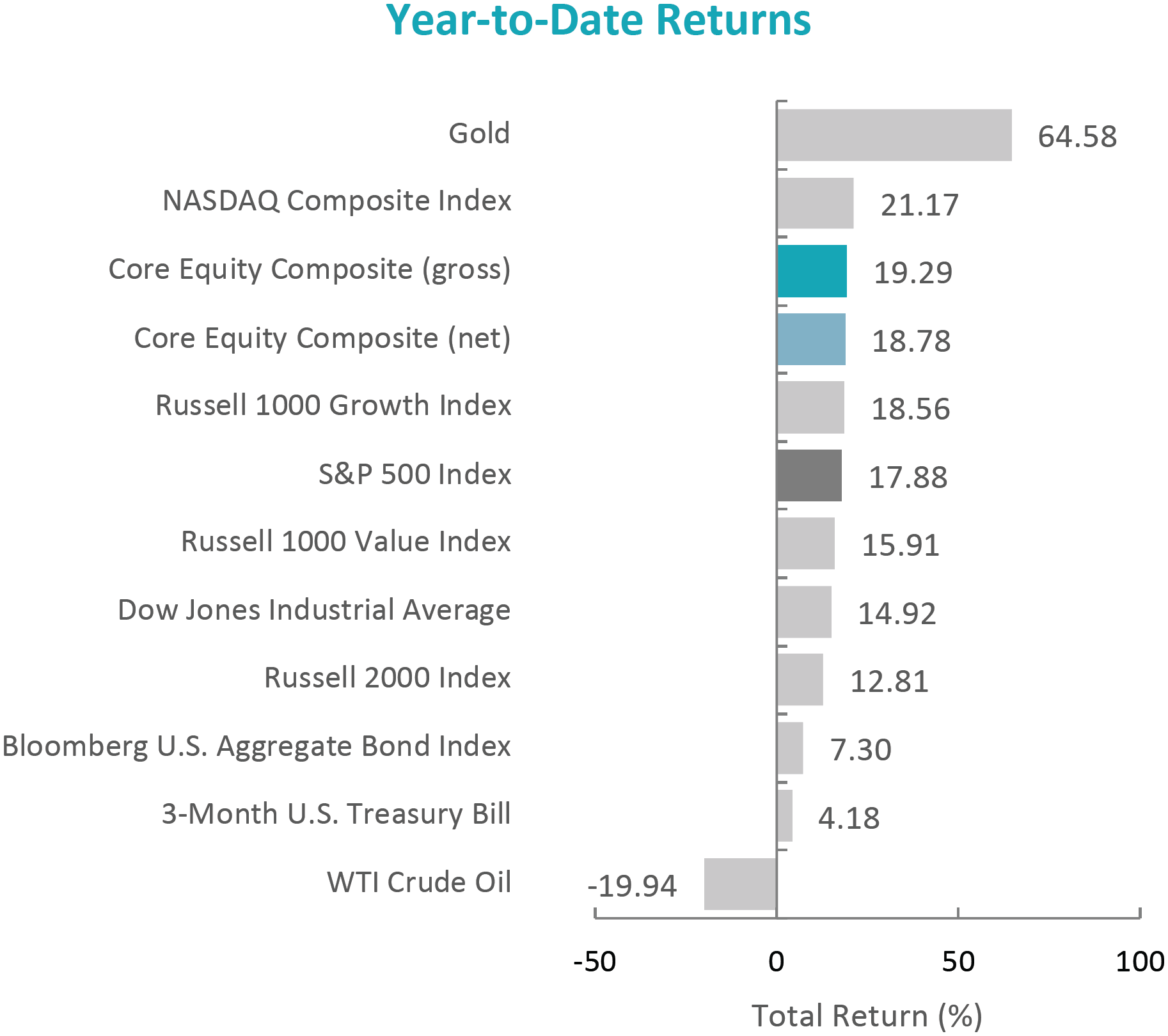

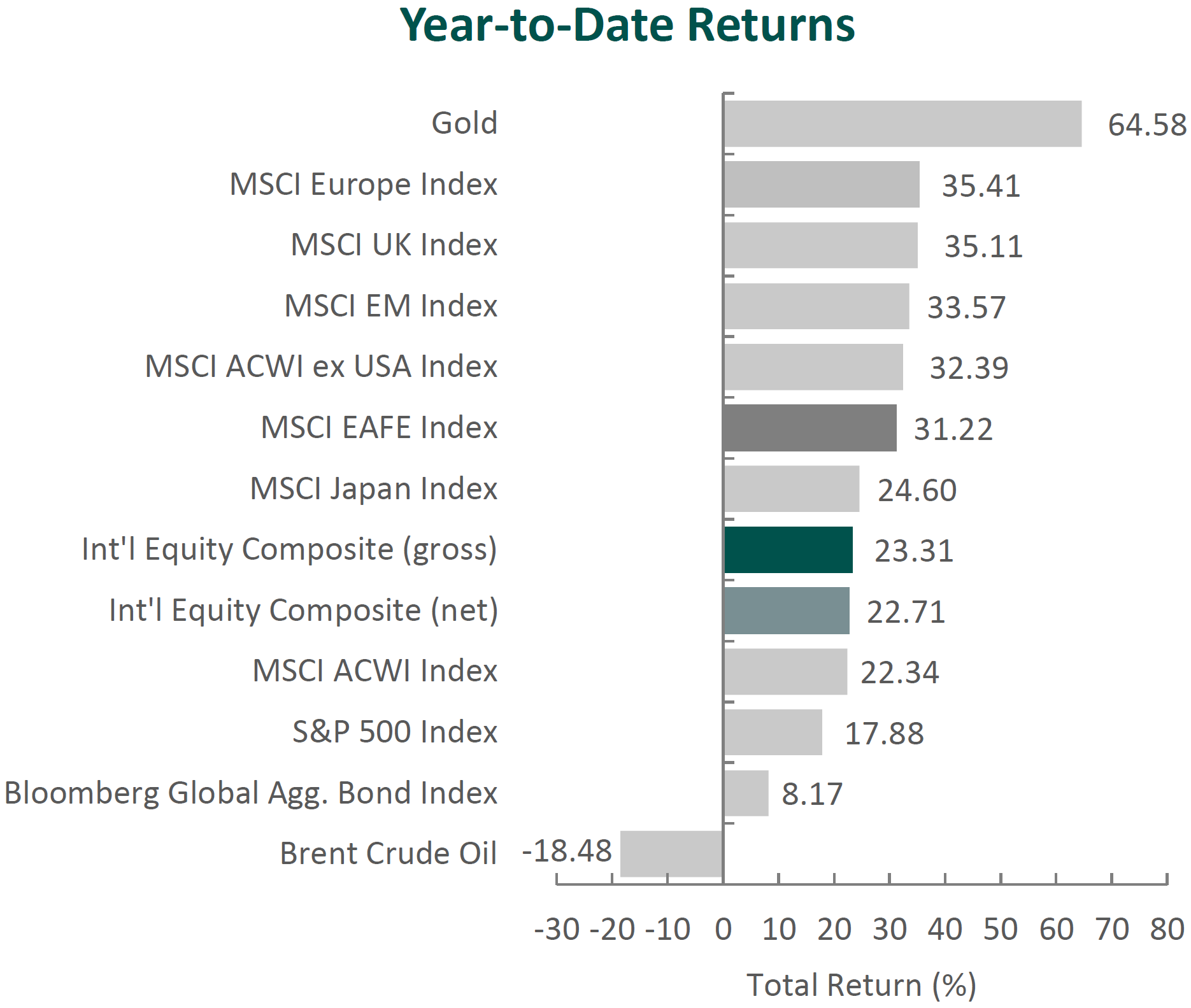

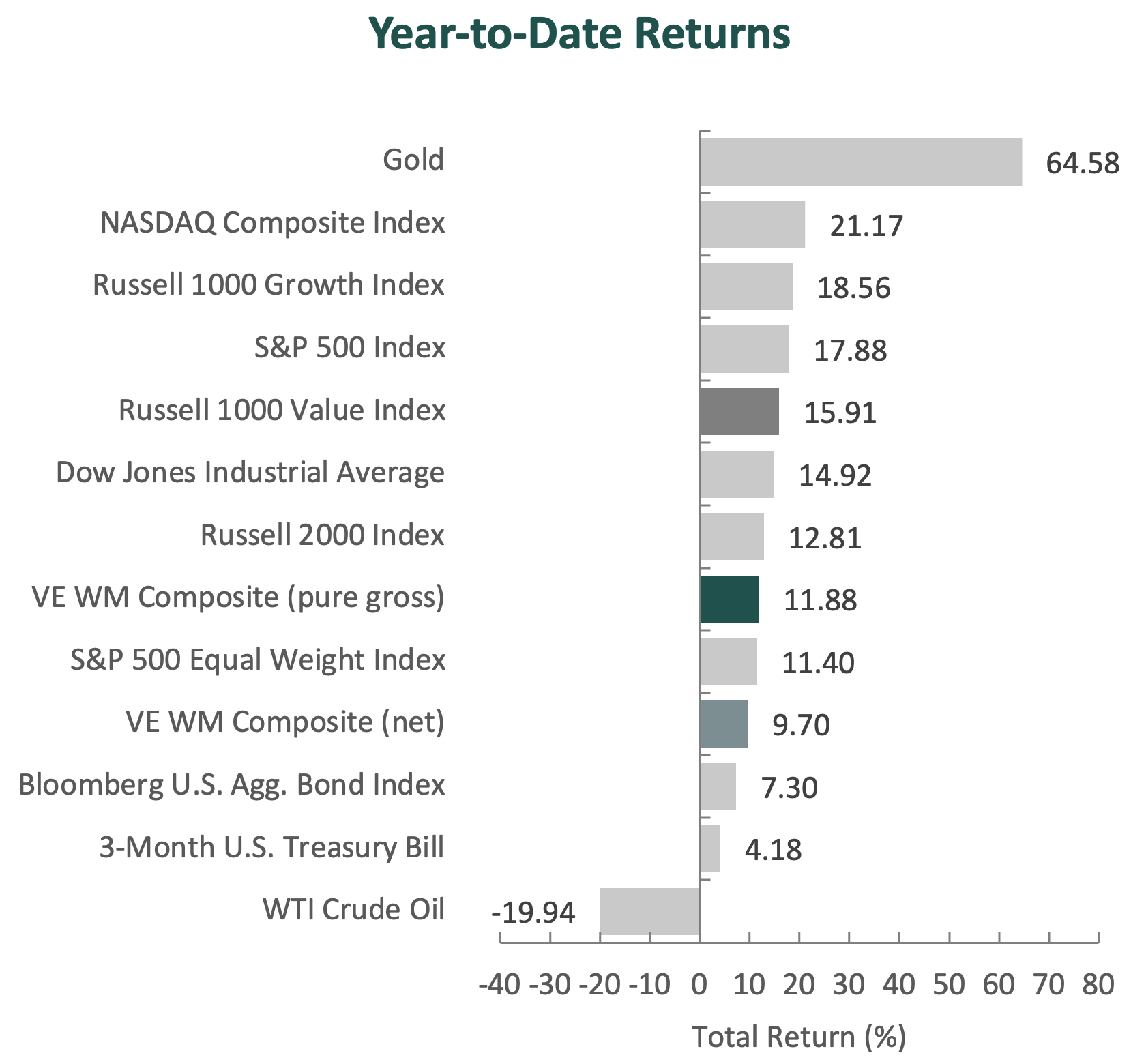

The U.S. equity markets extended their momentum in 2025, with the S&P 500 Index posting a full-year return of 17.88%. Similar to recent years, Communication Services and Information Technology were the strongest-performing sectors, rising 33.65% and 24.04%, respectively, as enthusiasm around AI remained a dominant market theme. Reflecting this leadership, the Russell 1000 Growth Index outperformed the Russell 1000 Value Index by 2.65% for the year.

Fixed income markets also delivered strong performance, with the Bloomberg U.S. Aggregate Bond Index advancing 7.30% over the period.

While trends such as AI continued to propel markets forward, 2025 was not without challenges, both new and existing. President Trump’s tariffs, ongoing geopolitical conflicts, mixed economic data and a government shutdown all contributed to heightened uncertainty.

Factors such as momentum and volatility outperformed quality, and while the economic and earnings backdrop was generally supportive, both the Fed and corporate management teams adopted a more cautious tone heading into 2026.

Given the risks and uncertainties surrounding macroeconomic conditions and market narratives, we believe it remains prudent to focus on individual businesses and their long-term fundamentals. By concentrating on what is analyzable, we believe our approach is well suited to navigating a range of market environments while remaining disciplined through full market cycles.

Performance and Attribution Summary

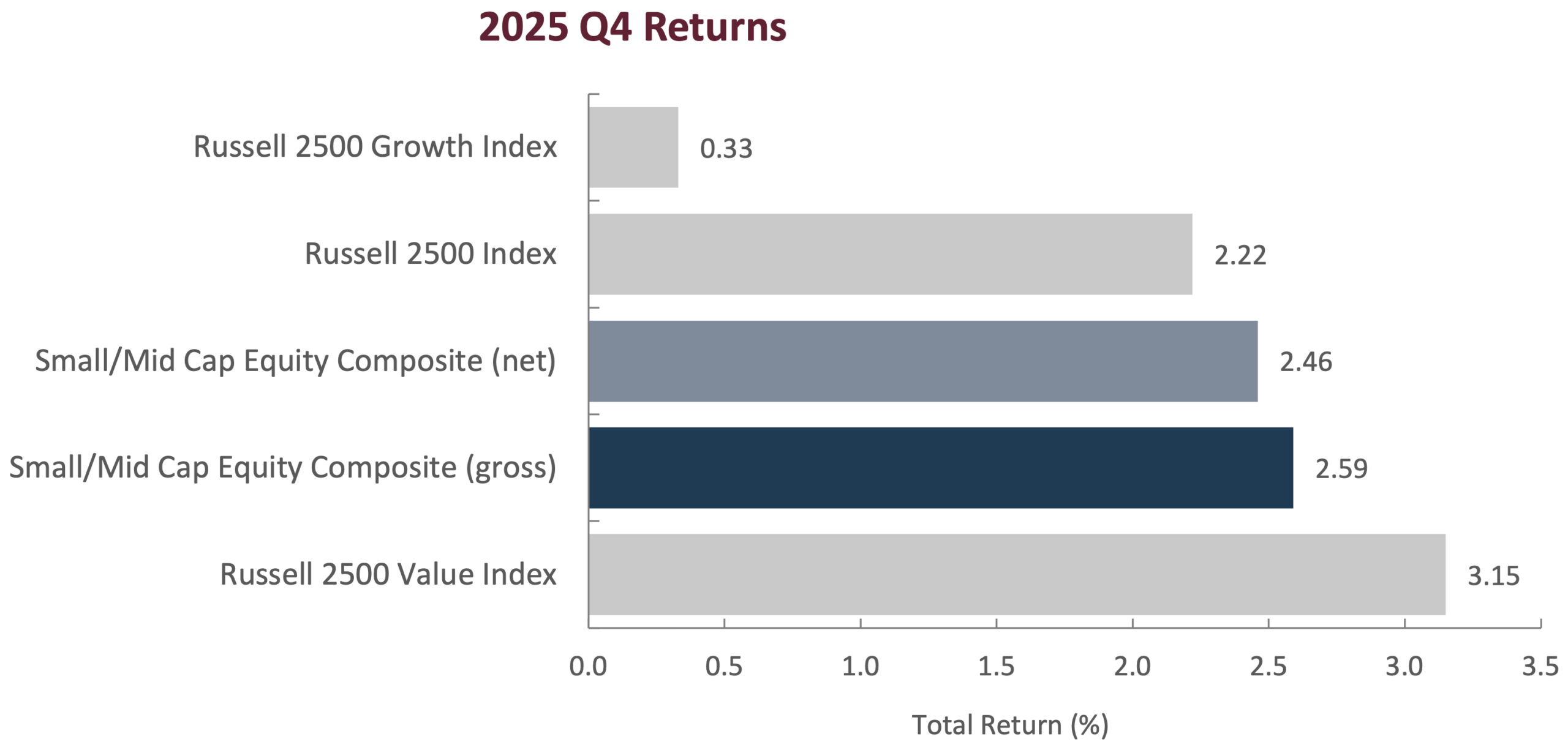

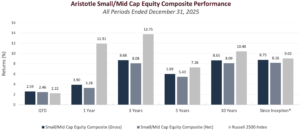

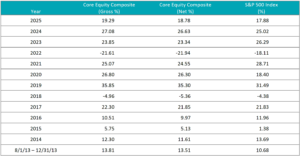

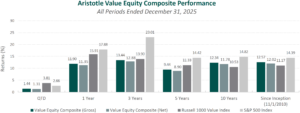

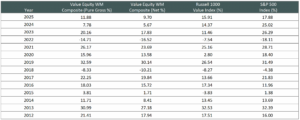

For the fourth quarter of 2025, Aristotle Capital’s Value Equity WM Composite posted a total return of 1.45% pure gross of fees (0.95% net of fees), underperforming the 3.81% return of the Russell 1000 Value Index and the 2.66% return of the S&P 500 Index. Please refer to the table for detailed performance.

| Performance (%) | 4Q25 | 1 Year | 3 Years | 5 Years | 10 Years |

|---|---|---|---|---|---|

| Value Equity WM Composite (pure gross) | 1.45 | 11.88 | 13.16 | 9.29 | 12.23 |

| Value Equity WM Composite (net) | 0.95 | 9.70 | 10.95 | 7.12 | 10.00 |

| Russell 1000 Value Index | 3.81 | 15.91 | 13.90 | 11.33 | 10.53 |

| S&P 500 Index | 2.66 | 17.88 | 23.01 | 14.47 | 14.82 |

Source: FactSet

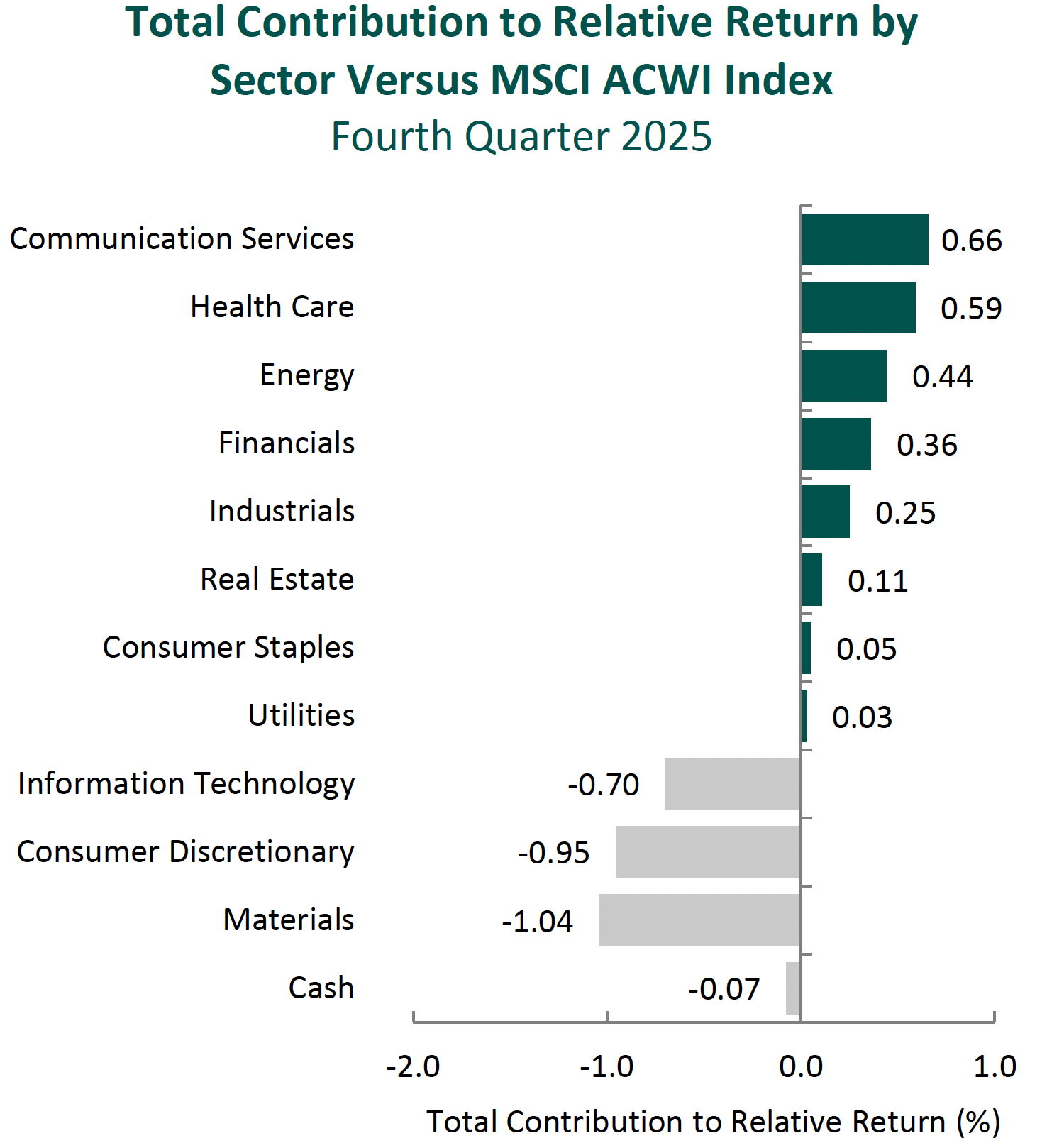

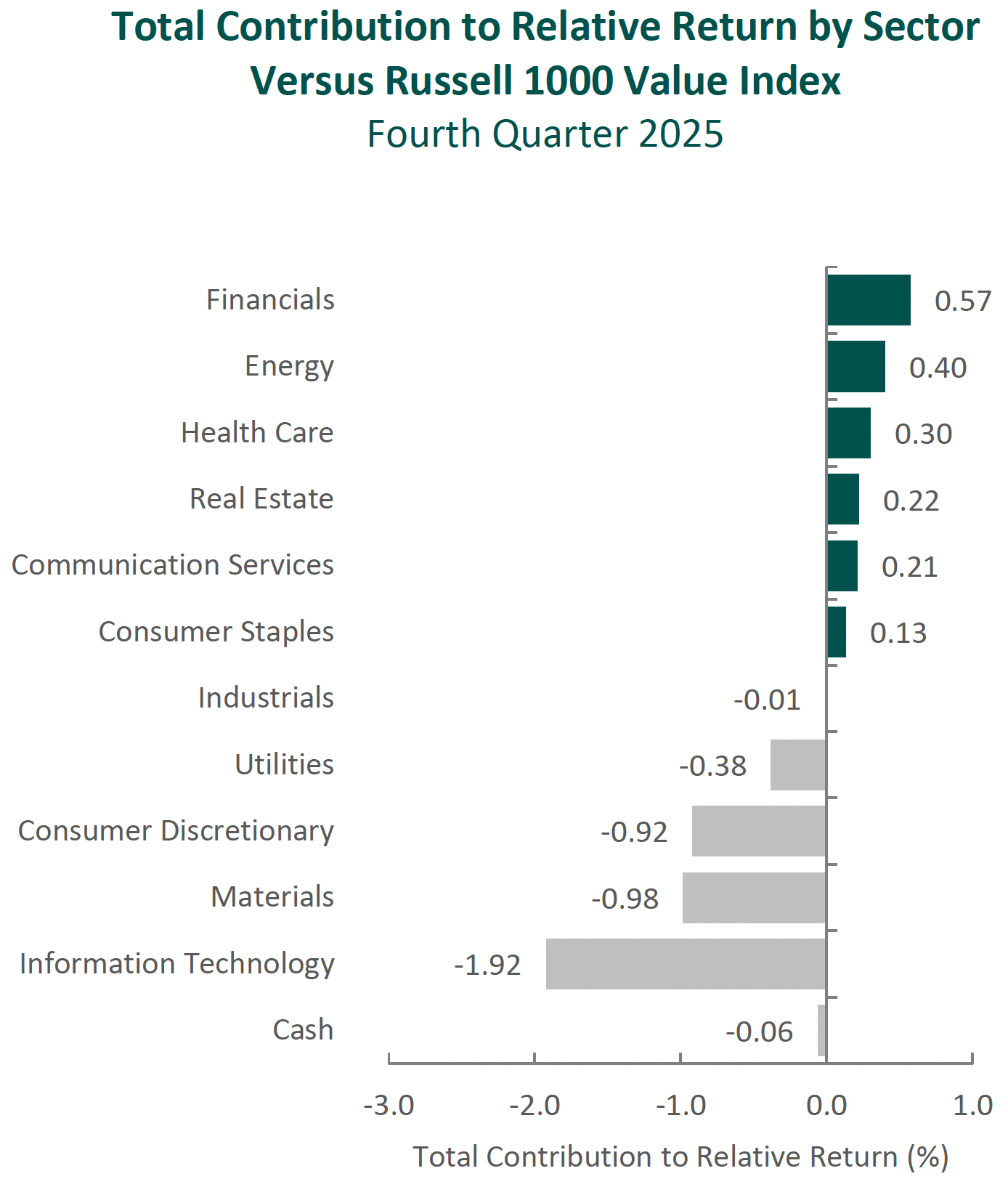

Past performance is not indicative of future results. Sector attribution shows how much of a portfolio’s overall return is directly attributable to stock selection and asset allocation decisions within the portfolio, highlighting which sectors contributed or detracted to the total return. Attribution includes the reinvestment of income. Attribution is presented gross of fees and does not include the deduction of all fees and expenses that a client or investor has paid or would have paid. Please refer to the pure gross and net composite returns included within to understand the overall impact of fees.

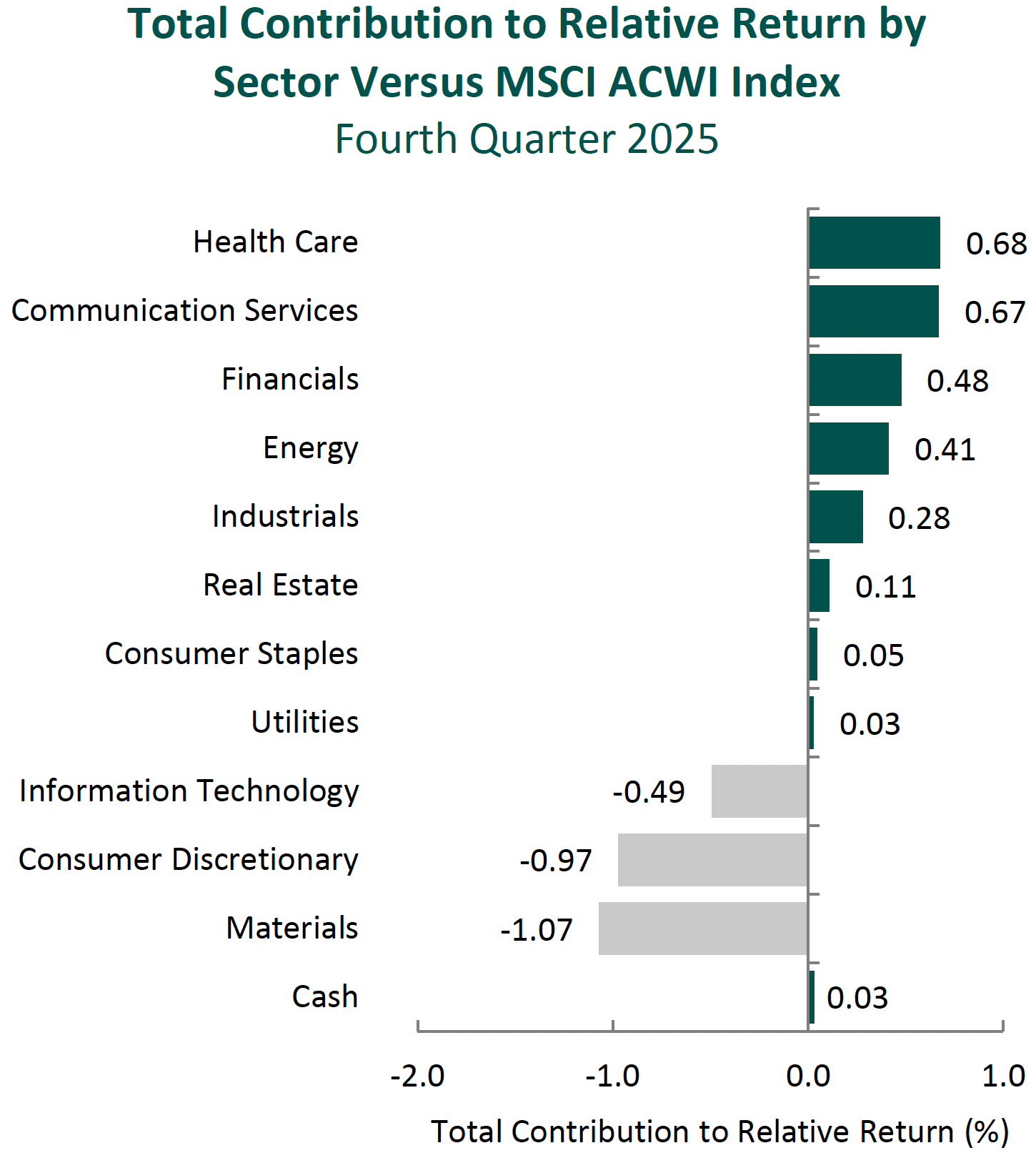

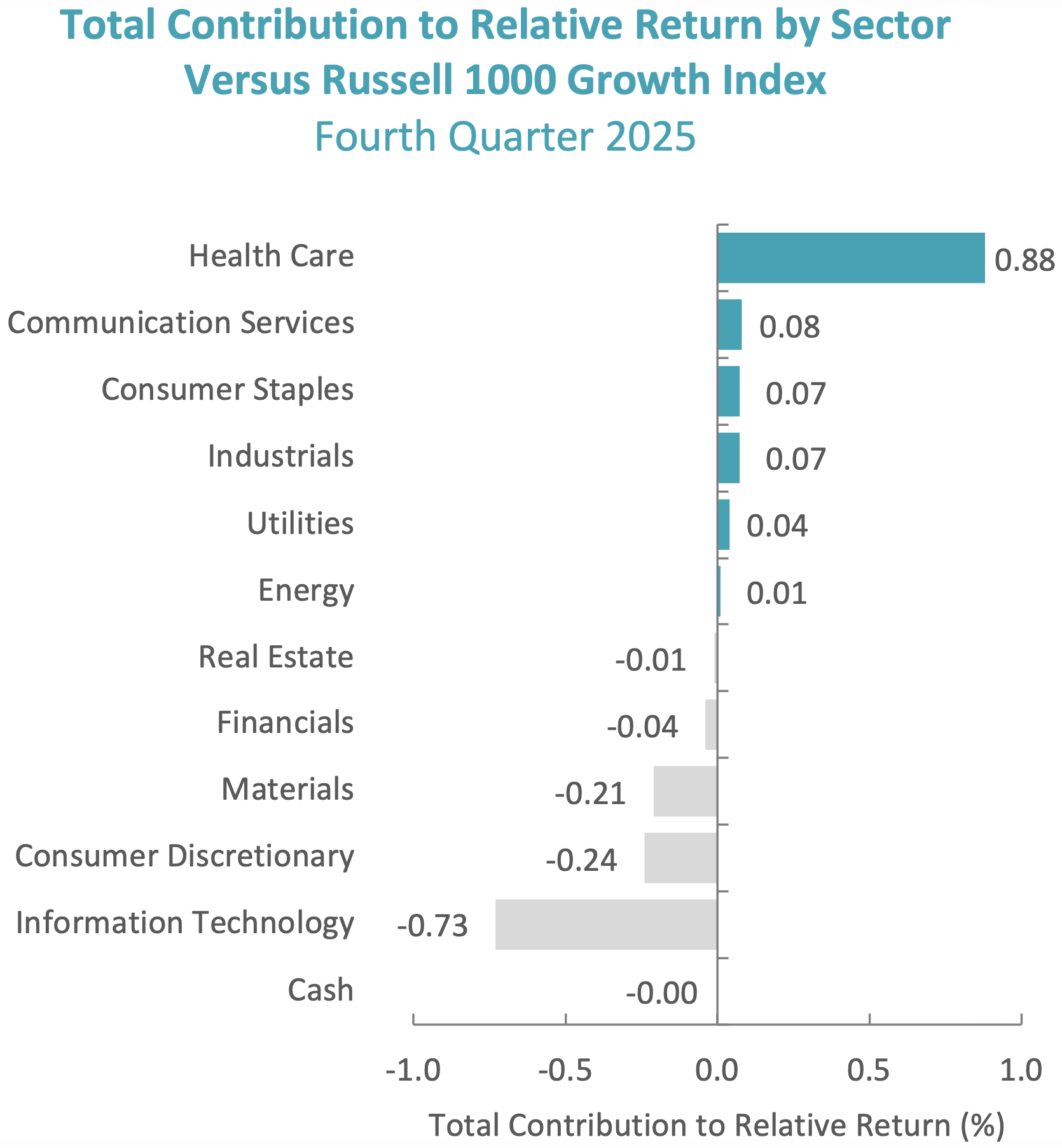

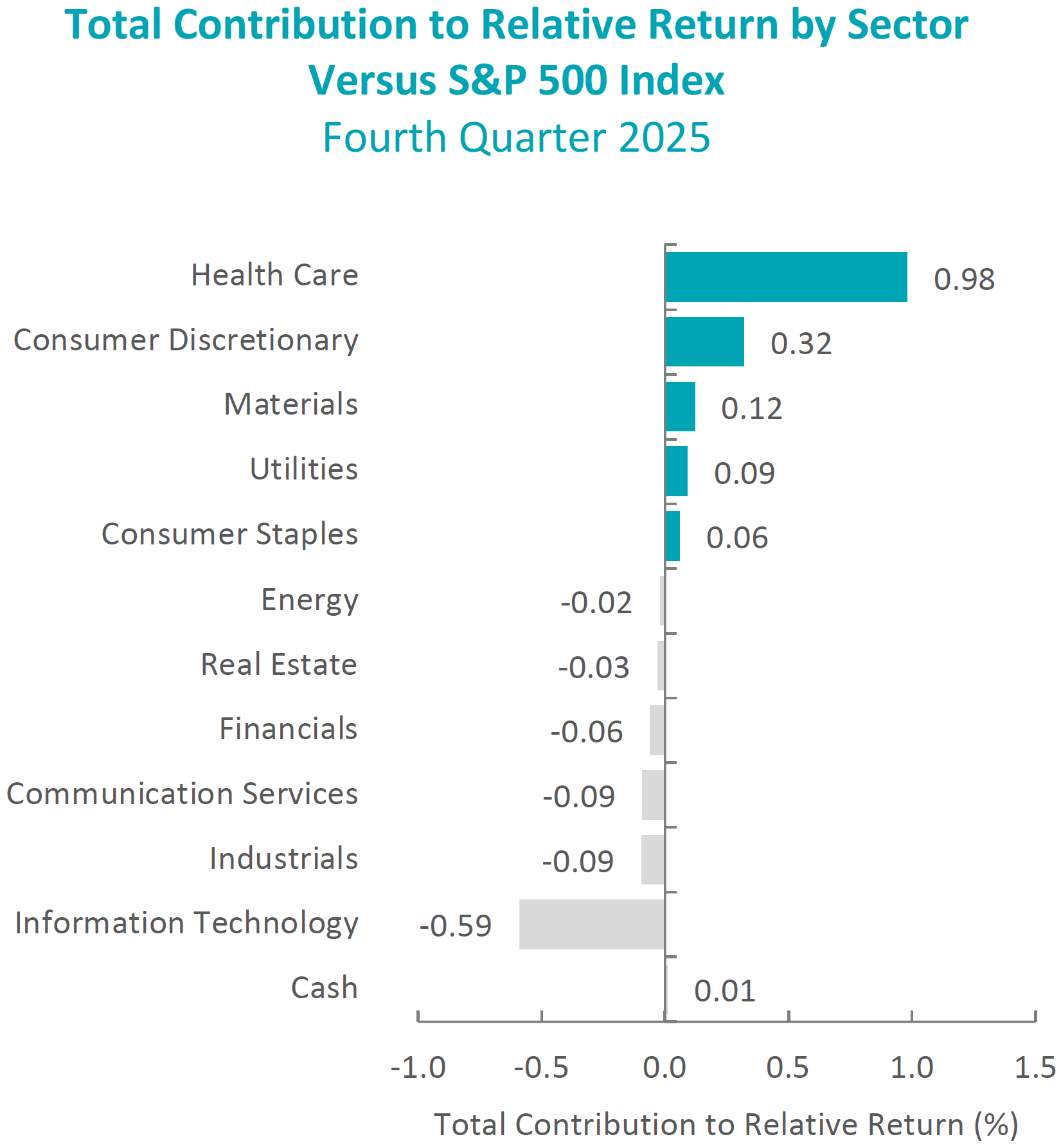

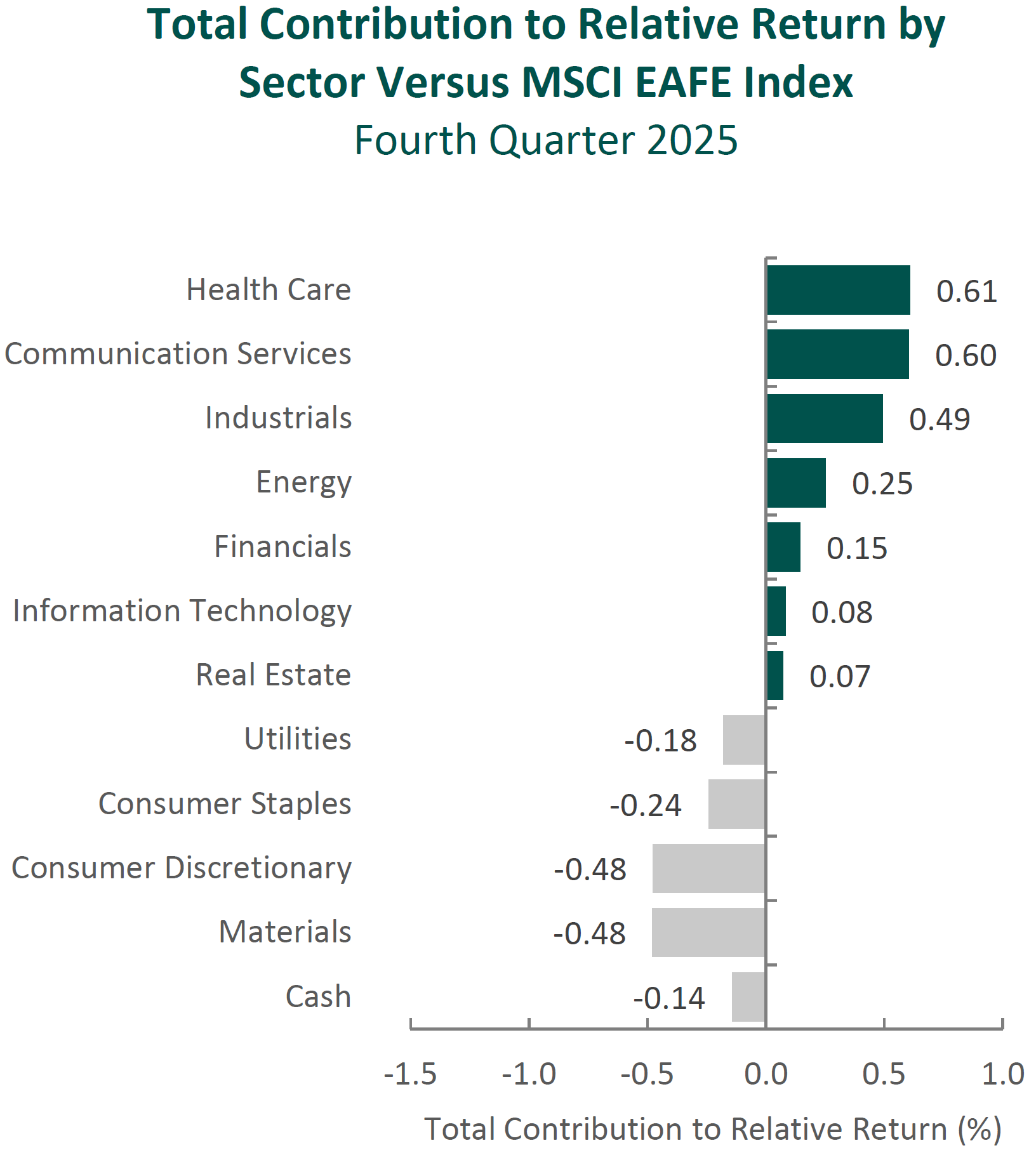

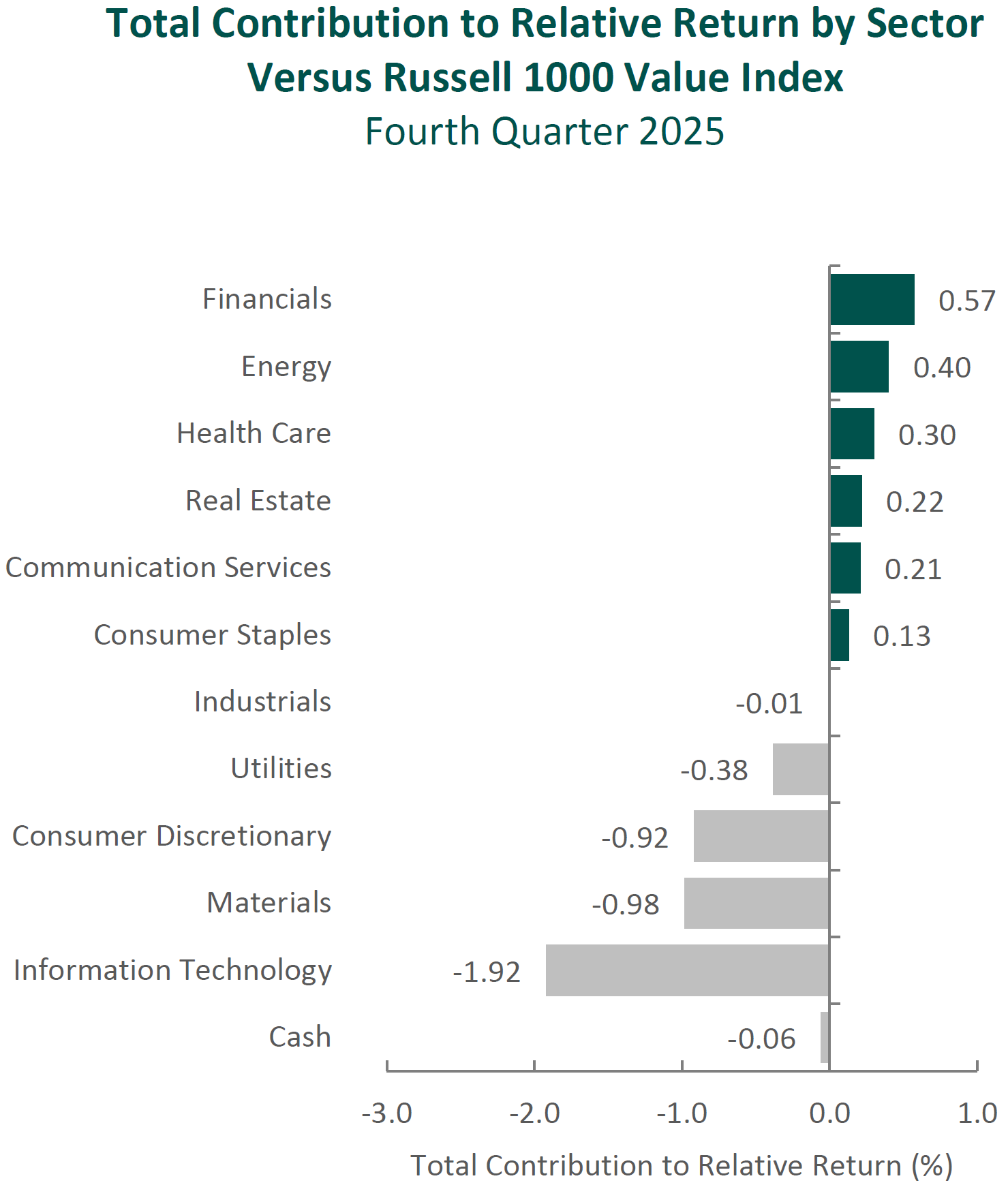

The portfolio’s underperformance relative to the Russell 1000 Value Index in the fourth quarter can be attributed to security selection, while allocation effects contributed. Security selection in Information Technology, Consumer Discretionary and Materials detracted the most from relative performance. Conversely, security selection in Financials, Health Care and Energy contributed. (Relative weights are the result of bottom-up security selection.)

Contributors and Detractors for 4Q 2025

| Relative Contributors | Relative Detractors |

|---|---|

| Parker Hannifin | Lennar |

| Capital One Financial | Sony |

| Amgen | Uber |

| Merck | Microsoft |

| U.S. Bancorp | Teledyne Technologies |

Sony, the global leader in video games, image sensors, music and movies, was a primary detractor for the period. Shares declined following the recognition of a one-time, non-cash charge of approximately ¥50 billion in the Game & Network Services segment related to an impairment and accounting correction of previously capitalized development costs. Importantly, this charge was not recurring and did not reflect a deterioration in underlying operating performance. Excluding this item, operating income would have increased approximately 23% year-over-year, supported by healthy gaming engagement, continued growth in network services and software sales, and strong results in the Music segment driven by streaming growth and recent theatrical releases. The company’s image sensor business also benefited from a favorable product mix and steady end-market demand. Looking ahead, we continue to see opportunity for Sony to capitalize on its unique position as both a content creator and platform owner. The company’s ability to integrate gaming, music, anime and film—and to leverage IP across its ecosystem—supports sustained engagement and recurring revenue. In addition, the recent spinoff of Sony’s Financial Services segment further sharpens management’s focus on its core content, technology and entertainment operations. We believe Sony’s industry leadership and continued focus on operational execution position the company well for long-term value creation.

Uber, a leading rideshare, delivery and shipping technology platform, was one of the largest detractors during the period. Trip volumes reached record levels, and gross bookings grew significantly year-over-year, yet the stock underperformed as investor focus shifted from growth to margin trajectory, regulatory risk and autonomous vehicle (AV) uncertainty. The primary near-term concern among market participants was management’s guidance around profitability. While results exceeded expectations on bookings and FREE cash flow, Uber signaled a deliberate moderation in margin expansion, as incremental profits are reinvested into affordability, cross-platform engagement and early AV initiatives. Regulatory concerns also resurfaced, particularly in Europe, where ongoing debates around driver classification and data protection continue to pose potential cost (and therefore margin) headwinds. At the same time, competitive anxiety around AVs intensified following Lyft’s expanded partnership with Waymo and continued investor focus on Tesla’s long-term robotaxi ambitions. Management acknowledged that autonomous initiatives will pressure near-term margins, as Uber invests to build supply and data infrastructure, even as utilization in early AV markets has been encouraging. Over the long term, however, our thesis remains intact. Uber’s global scale, deepening network effects, growing FREE cash flow and expanding cross-platform ecosystem position the company to compound value as profitability improves and new mobility technologies mature.

Parker Hannifin, the manufacturer of motion and control technologies, was the top contributor during the quarter. The company continues to benefit from strength in its aerospace business, where demand for original equipment and aftermarket services has driven organic growth and margin expansion. The ongoing integration of Meggitt, which Parker Hannifin acquired in 2022, has further expanded the company’s aerospace and defense capabilities while increasing exposure to higher-margin aftermarket revenue—a catalyst we previously identified. Alongside this progress, management has continued to strengthen the company’s balance sheet following a period of elevated acquisition activity, with net debt-to-EBITDA trending lower. In addition, Parker Hannifin’s broad portfolio of motion and control technologies positions the company to benefit from secular trends such as factory automation, electrification of industrial equipment, digitization, and increased complexity and modernization across commercial and defense aerospace platforms. The company continues to execute its Win Strategy, driving operational excellence, pricing discipline and strong cash flow generation. We believe these catalysts support a more resilient earnings profile and will allow Parker Hannifin to continue improving profitability and FREE cash flow generation over time.

Capital One Financial was a primary contributor during the quarter. Following the completion of its all-stock acquisition of Discover, the company reported strong results in its first full quarter post-transaction, including net interest margin expansion driven primarily by the addition of Discover’s credit card portfolio. The acquisition positions Capital One as one of the largest U.S. credit card issuers and adds ownership of the Discover payment network, which we believe has the potential to improve payment economics and enhance operating leverage over time. During the quarter, the company also announced increased capital returns through a new share buyback program and a higher quarterly dividend, reflecting confidence in its balance sheet and earnings power. In addition, resilient consumer spending, stable credit quality and a strengthening deposit base contributed to performance. We believe Capital One’s scale and integrated payments capabilities support a more resilient earnings profile and position the company to continue generating attractive returns over time.

Recent Portfolio Activity

| Buys | Sells |

|---|---|

| None | Commerce Bancshares |

| Constellation Brands | |

| Sony Financial |

During the quarter, we sold our positions in Commerce Bancshares, Constellation Brands and Sony Financial.

We first invested in Commerce Bancshares, the Kansas City-based bank, in the fourth quarter of 2019. We were attracted to the bank’s conservatively run franchise, disciplined approach to credit, well-diversified revenue mix with a meaningful contribution from fee-based businesses, and long-tenured management team that has historically operated with a “private company” mindset. At the time of purchase, we identified several catalysts, including continued loan growth—particularly in core Kansas markets—prudent expense management, sustained strong credit underwriting, and the accretive deployment of excess capital through dividends and share repurchases. Over our holding period, Commerce executed consistently against these objectives, demonstrating resilience through multiple operating environments while maintaining strong credit quality, disciplined cost control and steady capital returns, including a long history of dividend increases. As these catalysts played out, we chose to sell our position and redeployed the proceeds into what we view as a more attractive investment opportunity in Wells Fargo, which we purchased in the third quarter of 2025.

We first invested in Constellation Brands, the premium beer, wine and spirits company, in the fourth quarter of 2021. At the time, we believed the company was well positioned to benefit from its dominant share of the fast-growing Mexican imports segment of U.S. beer, supported by iconic brands such as Modelo, Corona and Pacifico, hard-to-replicate production assets in Mexico, and a management team with a strong track record of building brands and marketing imported brands to mainstream U.S. consumers and expanding distribution. Over our holding period, Constellation continued to benefit from the growing popularity of Mexican beer in the U.S and its core beer segment remained a clear source of strength. However, the timing and magnitude of several key catalysts evolved. Expansion of shelf space and overall distribution progressed more slowly than expected, while improvement in the Wine & Spirits segment proved more challenging, pushing meaningful margin recovery further into the future. As a result, while the long-term strategic rationale for the business remains intact, we determined that Constellation was the most appropriate candidate for sale to fund a new investment in the first quarter of 2026, to be discussed in greater detail next quarter.

We received shares of Sony Financial following its spinoff from our long-term holding Sony in October 2025. Sony Financial is a Japan-based financial services company with operations in life insurance, banking and digital payments. While we view Sony Financial as an attractive, well-managed business, its operations are focused primarily on the Japanese market. Given this focus, we elected to sell the shares received in the spinoff.

Conclusion

Markets and economic conditions will continue to evolve, often in ways that are difficult to anticipate. While we remain attentive to these developments, our work is ultimately centered on understanding individual businesses—how they compete, how they allocate capital and how their economics change over time. We recognize that progress in business fundamentals and investment outcomes do not always align over shorter periods. Thus, we approach our investment process with patience and a willingness to reassess our views as circumstances change. Rather than react impulsively to every macro headline or try to time short-term market moves, we focus on what is analyzable and enduring: the long-term fundamentals of the companies we own. We believe this careful, fundamental approach remains the most reliable way to add value for our clients over the long run, across a wide range of market environments.

The opinions expressed herein are those of Aristotle Capital Management, LLC (Aristotle Capital) and are subject to change without notice. Past performance is not a guarantee or indicator of future results. This material is not financial advice or an offer to purchase or sell any product. You should not assume that any of the securities transactions, sectors or holdings discussed in this report were or will be profitable, or that recommendations Aristotle Capital makes in the future will be profitable or equal the performance of the securities listed in this report. The portfolio characteristics shown relate to the Aristotle Value Equity strategy. Not every client’s account will have these characteristics. Aristotle Capital reserves the right to modify its current investment strategies and techniques based on changing market dynamics or client needs. There is no assurance that any securities discussed herein will remain in an account’s portfolio at the time you receive this report or that securities sold have not been repurchased. The securities discussed may not represent an account’s entire portfolio and, in the aggregate, may represent only a small percentage of an account’s portfolio holdings. The performance attribution presented is of a representative account from Aristotle Capital’s Value Equity strategy. The representative account is a discretionary client account which was chosen to most closely reflect the investment style of the strategy. The criteria used for representative account selection is based on the account’s period of time under management and its similarity of holdings in relation to the strategy. Recommendations made in the last 12 months are available upon request.

Composite returns are presented pure gross and net of the maximum wrap fee and include the reinvestment of all income. Pure gross returns do not reflect the deduction of any trading costs or other fees and are supplemental to the net returns. Net returns are calculated by subtracting the highest applicable wrap/SMA fee, which includes trading costs and custodial fees, from the pure gross composite return. (From inception to 12/31/2015, the highest applicable wrap/SMA fee is 3.00% on an annual basis, or 0.75% quarterly. From 1/1/2016 to 12/31/2023, the highest applicable wrap/SMA fee is 2.00% on an annual basis, or 0.50% quarterly and 0.17% monthly from 1/1/2024 to present.)

All investments carry a certain degree of risk, including the possible loss of principal. Investments are also subject to political, market, currency and regulatory risks or economic developments. International investments involve special risks that may in particular cause a loss in principal, including currency fluctuation, lower liquidity, different accounting methods and economic and political systems, and higher transaction costs. These risks typically are greater in emerging markets. While Large-capitalization companies may have more stable prices than smaller, less established companies, they are still subject to equity securities risk. In addition, large-capitalization equity security prices may not rise as much as prices of equity securities of small-capitalization companies. Securities of small- and medium-sized companies tend to have a shorter history of operations and be more volatile and less liquid. Value stocks can perform differently from the market as a whole and other types of stocks. The material is provided for informational and/or educational purposes only and is not intended to be and should not be construed as investment, legal or tax advice and/or a legal opinion. Investors should consult their financial and tax adviser before making investments. The opinions referenced are as of the date of publication, may be modified due to changes in the market or economic conditions, and may not necessarily come to pass. Information and data presented has been developed internally and/or obtained from sources believed to be reliable. Aristotle Capital does not guarantee the accuracy, adequacy or completeness of such information.

Aristotle Capital Management, LLC is an independent registered investment adviser under the Advisers Act of 1940, as amended. Registration does not imply a certain level of skill or training. More information about Aristotle Capital, including our investment strategies, fees and objectives, can be found in our ADV Part 2, which is available upon request. ACM-2601-92

Composite returns for all periods ended December 31, 2025 are preliminary pending final account reconciliation.

Past performance is not indicative of future results. The information provided should not be considered financial advice or a recommendation to purchase or sell any particular security or product. Performance results for periods greater than one year have been annualized.

The Aristotle Value Equity WM Composite has an inception date of 10/1/1979. As of 1/1/2024, the Composite was renamed from the Value Equity Wrap Composite and the inception date was updated to 1/1/2012. This update was implemented to align the start date of the composite track record with the start date of the current decision maker. Performance achieved by the firm prior to that date is available upon request.

Composite returns are presented pure gross and net of the maximum wrap fee and include the reinvestment of all income. Pure gross returns do not reflect the deduction of any trading costs or other fees and are supplemental to the net returns. Net returns are calculated by subtracting the highest applicable wrap/SMA fee, which includes trading costs and custodial fees, from the pure gross composite return. (From inception to 12/31/2015, the highest applicable wrap/SMA fee is 3.00% on an annual basis, or 0.75% quarterly. From 1/1/2016 to 12/31/2023, the highest applicable wrap/SMA fee is 2.00% on an annual basis, or 0.50% quarterly and 0.17% monthly from 1/1/2024 to present.)

The Russell 1000® Value Index measures the performance of the large cap value segment of the U.S. equity universe. It includes those Russell 1000 Index companies with lower price-to-book ratios and lower expected growth values. The S&P 500® Index is the Standard & Poor’s Composite Index of 500 stocks and is a widely recognized, unmanaged index of common stock prices. The S&P 500 Equal Weight Index is designed to be the size-neutral version of the S&P 500. It includes the same constituents as the cap-weighted S&P 500, but each company in the S&P 500 Equal Weight Index is allocated the same weight at each quarterly rebalance. The Russell 1000® Growth Index measures the performance of the large cap growth segment of the U.S. equity universe. It includes those Russell 1000 companies with higher price-to-book ratios and higher forecasted growth values. The Russell 2000® Index measures the performance of the small cap segment of the U.S. equity universe. The Russell 2000 Index is a subset of the Russell 3000® Index representing approximately 10% of the total market capitalization of that index. It includes approximately 2,000 of the smallest securities based on a combination of their market cap and current index membership. The Dow Jones Industrial Average® is a price-weighted measure of 30 U.S. blue-chip companies. The Index covers all industries except transportation and utilities. The NASDAQ Composite Index measures all NASDAQ domestic and international based common type stocks listed on The NASDAQ Stock Market. The NASDAQ Composite includes over 3,000 companies, more than most other stock market indexes. The Bloomberg U.S. Aggregate Bond Index is an unmanaged index of domestic investment grade bonds, including corporate, government and mortgage-backed securities. The WTI Crude Oil Index is a major trading classification of sweet light crude oil that serves as a major benchmark price for oil consumed in the United States. The 3-Month U.S. Treasury Bill is a short-term debt obligation backed by the U.S. Treasury Department with a maturity of three months. The Consumer Price Index is a measure of the average change over time in the prices paid by urban consumers for a market basket of consumer goods and services. The volatility (beta) of the Composite may be greater or less than its respective benchmarks. It is not possible to invest directly in these indices.