It was September 24, 1966. The wealthy and well-connected Vanger family hosted a party at their home which took up much of Hedeby Island in northern Sweden. When it came time for dinner, the Patriarch of the family, Henrik Vanger, noticed an empty chair, that of his grandniece, 16-year-old Harriet. The next morning she was still missing at breakfast.

Frantic, the family literally called out the dogs and a massive search of the island ensued. She was not to be found. “No, she would not have just run off like that. We were too close; how shameful I was for not taking those few seconds to speak with her that day when she asked to see me. She must have been in trouble, and I could have protected her. No, it’s foul play for certain. ALL her belongings were still in her room, surrounding her bed, unslept in.”

Fast forward to the year 2005, Stockholm, Sweden. It was a typically cold and frosty winter. Henrik Vanger never lost his devotion to finding out what happened to (likely who killed) Harriet on that day she went missing. He noticed on the evening news one day a report that Swedish journalist – and part owner of the small, but acclaimed, Millennium Magazine – Mikael Blomkvist, had lost a libel suit, not being able to sufficiently prove allegations made against a local businessman. “This is going to bankrupt the Millennium,” said Henrik to his friend, confidante and legal counsel, standing by his side. “Go hire that Blomkvist. He’s one helluva good investigative journalist. Perhaps he can figure out whatever happened to Harriet.”

To read the full article, please use the link below.

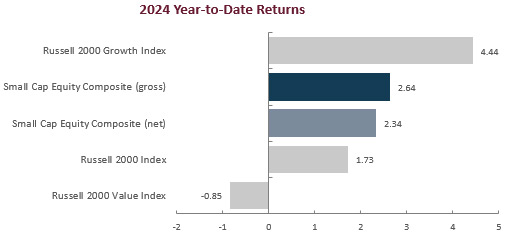

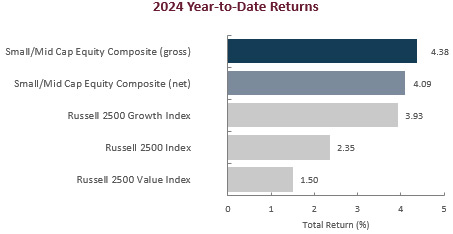

Small caps gave back some of their first quarter gains with the Russell 2000 index delivering a total return of -3.28%. Potential slowing in the US economy weighed on investor sentiment but lent credence to a soft landing scenario in 2024. The Consumer Price Index (CPI) drifted lower during the quarter, coming in below expectations at 3.0% as inflationary pressures have eased. Employment was muddled during the period as non-farm payroll growth was positive but volatile while unemployment steadily climbed to 4.1%. Despite softening data, the Federal Reserve (Fed) held its ground on easing at its June meeting, forecasting only one Fed funds rate cut in 2024, down from 3 cuts from its March meeting. The U.S. Treasury yield curve steepened with the yield on the 10-year note rising 16 basis points (bps) to end June at 4.36%.

Stylistically, growth stocks outperformed their value counterparts during the quarter as evidenced by the Russell 2000 Growth Index returning -2.92% compared to -3.64% for the Russell 2000 Value Index. There were three sectors that posted a positive absolute return in the growth index while all sectors in the value index were negative. Two of the largest names in the growth index for the first quarter, Super Micro and MicroStrategy, were the worst performers in the second quarter. Whether the underperformance was a function of decreasing AI enthusiasm or selling in advance of the two companies graduating to the larger Russell 1000 Index, it’s fair to say that the concentration and performance impact from both companies will be discussed by active small cap managers and academics for years to come. Pockets of exuberance can still be seen in the small cap universe as noted by the fact that Carvana, a volatile used car selling platform that had completed a distressed debt exchange in the fall of 2023, was the top contributor in the Russell 2000 Value Index as well as a top contributor in the Growth Index.

At the sector level, only two of the eleven sectors in the Russell 2000 Index recorded positive returns during the second quarter, led by the Consumer Staples (+2.28%), Utilities (+0.13%), and Communication Services (-0.63%) sectors. Conversely, Consumer Discretionary (-5.99%), Industrials (-4.41%), and Health Care (-4.29%) all lagged. Looking at market factors, profitable companies outperformed loss makers by nearly 200 bps during the quarter.

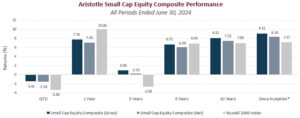

Sources: CAPS Composite Hub, Russell Investments Past performance is not indicative of future results. Returns are presented gross and net of investment advisory fees and include the reinvestment of all income. Gross returns will be reduced by fees and other expenses that may be incurred in the management of the account. Net returns are presented net of actual investment advisory fees and after the deduction of all trading expenses. Aristotle Small Cap Equity Composite returns are preliminary pending final account reconciliation. Please see important disclosures at the end of this document.

Performance Review

For the second quarter of 2024, the Aristotle Small Cap Equity Composite posted a total return of -1.56% net of fees (-1.41% gross of fees), outperforming the -3.28% total return of the Russell 2000 Index. Outperformance was primarily driven by security selection while allocation effects also contributed. Overall, security selection was strongest within the Information Technology, Energy, and Financials sectors and weakest in Consumer Discretionary, Health Care, and Materials. From an allocation perspective, the portfolio benefitted from an underweight in Consumer Discretionary and an overweight in Information Technology, however, this was partially offset by an overweight in Industrials and an underweight in Financials.

Relative Contributors

Relative Detractors

Ardmore Shipping

Carter’s

Dycom Industries

Cerence

Baldwin Insurance Group

Acadia Healthcare

TKO Group Holdings

Charles River Laboratories

Benchmark Electronics

The AZEK Company

CONTRIBUTORS

Ardmore Shipping (ASC), a product and chemical transportation company focused on modern mid-sized vessels, appreciated amid global refinery shifts and geopolitical factors, boosted voyage lengths and demand for product tankers. We maintain a position, as we believe the company continues to operate from a position of strength, driven by recent shareholder-friendly capital allocation decisions, strong operating performance, and a favorable industry supply-demand backdrop.

Dycom Industries (DY), a provider of engineering and construction services to the telecommunications and cable television industries, benefitted from continued growth in its core business, funding tailwinds, and expanding margins as demand for wireline services continues to grow. We maintain a position as we believe the company remains well positioned for longer-term growth alongside secular trends for expanding fiber deployments to support faster broadband connectivity speeds and opportunities to deploy fiber to rural or underserved areas across the country.

DETRACTORS

Carter’s (CRI), a leading marketer of baby and young children’s apparel in North America, declined amid a cautious consumer spending environment and weak direct-to-consumer trends for the business during the quarter. We maintain our position as we believe the company has a strong brand in a stable category and that store rationalization efforts and an improving demographic backdrop can drive a sales recovery in the business in periods to come.

Cerence (CRNC), a developer of voice-connected technology for the transportation market, declined after guiding down the full-year revenue forecast along with the CFO’s departure. As discussed later, the investment team decided to sell the full position during the quarter.

Recent Portfolio Activity

Buys/Acquisitions

Sells/Liquidations

Chart Industries

AZZ

Littelfuse

Cerence

PowerSchool

BUYS/ACQUISITIONS

Chart Industries (GTLS), an industrial equipment manufacturer that provides cryogenic equipment for storage, distribution, and other processes within the industrial gas and LNG, hydrogen, helium, carbon capture and water treatment industries was added to the portfolio. Strong forward demand for LNG and accelerating hydrogen opportunities coupled with company-specific improvement initiatives should benefit the company moving forward.

Littelfuse (LFUS), a designer and manufacturer of circuit protection, power control, and sensing products for the automotive, industrial, medical, and consumer end markets, was added to the portfolio. We believe the company’s dominant position in circuit protection and growing presence in automotive sensors and power semiconductors/components should benefit from ongoing efforts to solve power control and connection problems between the digital and physical worlds.

SELLS/LIQUIDATIONS

AZZ (AZZ), a provider of hot dip galvanizing and coil coating solutions, was sold during the quarter as the company’s stock price appreciated significantly since our initial purchase causing the reward to risk ratio to compress.

Cerence (CRNC), a provider of speech recognition and voice technologies for automotive applications was sold as the company embarked on a strategic shift to capitalize on the AI opportunity disrupting the financial progress we were anticipating.

PowerSchool (PWSC), a leading provider of cloud-based software for K-12 education in North America, was removed from the portfolio following the announcement the company was being taken private by investment firm Bain Capital.

Outlook

We continue to remain optimistic about the long-term potential for the small-cap segment of the U.S. market as valuations and potential tailwinds bode well for the asset class. As we look out to the second half of 2024, we are cautiously constructive as encouraging signs of economic stability are balanced by now consensus expectations of a soft landing scenario and the pricing of risk. So, despite greater clarity over the Fed’s path from here, there remains a long list of items creating uncertainty that could lead to greater volatility in 2024 including, but not limited to, signs that inflationary pressures have not yet fully dissipated, geopolitical tensions, U.S. equity index concentration issues, ongoing commercial real estate and regional banking concerns, and the looming presidential election. We are well aware that most of these issues are well known, but the timing and magnitude of the impact of any and all of these issues remains unpredictable. Therefore, as we always have, we will continue to avoid the temptation to forecast their outcome in favor of assessing the potential impact from a range of potential outcomes within our company‐specific, bottom-up analysis, and quality focus.

From an asset class perspective, valuations of small versus large continue to remain near multi-decade lows, which we believe suggests a more favorable setup for small caps relative to large caps in the periods to come (15.6x P/E for the Russell 2000 Index vs. 24.8x P/E for the Russell 1000 Index). Against a backdrop of moderating inflation, normalized interest rates, and a still growing U.S. economy, it looks to us that small-cap’s stretch of underperformance has the potential to end. If the economy continues to stabilize, our view is that valuations are likely to rise for those businesses that have largely sat out the mega-cap performance regime. It also helps that the well-noted concentration in large caps is reaching 50-year highs and small cap valuation relative to large cap is at multi-decade lows, therefore any fundamentally driven repositioning is likely to benefit small caps more than larger companies, in our view. Lastly, we believe smaller caps remain better positioned to benefit from the reshoring of U.S. manufacturing, a pickup in M&A activity, the CHIPS Act, and several infrastructure projects on the horizon.

Positioning

Our current positioning is a function of our bottom-up security selection process and our ability to identify what we view as attractive investment candidates, regardless of economic sector definitions. Overweights in Industrials and Information Technology are mostly a function of our underlying company specific views rather than any top-down predictions for each sector. Conversely, we continue to be underweight in Consumer Discretionary, as we have been unable to identify what we consider to be compelling long-term opportunities that fit our discipline given the rising risk profiles of many retail businesses and a potential deceleration in goods spending following a period of strength. While the portfolio’s allocation to Health Care is modestly below that of the benchmark, we continue to remain underweight the Biotechnology industry as many companies within that group do not fit our discipline due to their elevated levels of binary risk. Given our focus on long-term business fundamentals, patient investment approach and low portfolio turnover, the strategy’s sector positioning generally does not change significantly from quarter to quarter. However, we may take advantage of periods of volatility by adding selectively to certain companies when appropriate.

Disclosures

The opinions expressed herein are those of Aristotle Capital Boston, LLC (Aristotle Boston) and are subject to change without notice.

Past performance is not indicative of future results. The information provided in this report should not be considered financial advice or a recommendation to purchase or sell any particular security. There is no assurance that any securities discussed herein will remain in an account’s portfolio at the time you receive this report or that securities sold have not been repurchased. The securities discussed may not represent an account’s entire portfolio and, in the aggregate, may represent only a small percentage of an account’s portfolio holdings. The performance attribution presented is of a representative account from Aristotle Boston’s Small Cap Equity Composite. The representative account is a discretionary client account which was chosen to most closely reflect the investment style of the strategy. The criteria used for representative account selection is based on the account’s period of time under management and its similarity of holdings in relation to the strategy. It should not be assumed that any of the securities transactions, holdings or sectors discussed were or will be profitable, or that the investment recommendations or decisions Aristotle Boston makes in the future will be profitable or equal the performance of the securities discussed herein. Aristotle Boston reserves the right to modify its current investment strategies and techniques based on changing market dynamics or client needs. Recommendations made in the last 12 months are available upon request.

Returns are presented gross and net of investment advisory fees and include the reinvestment of all income. Gross returns will be reduced by fees and other expenses that may be incurred in the management of the account. Net returns are presented net of actual investment advisory fees and after the deduction of all trading expenses.

Effective January 1, 2022, the Aristotle Small Cap Equity Composite has been redefined to exclude accounts with meaningful industry-specific restrictions or substantial values-based screens hampering implementation of the small cap strategy.

All investments carry a certain degree of risk, including the possible loss of principal. Investments are also subject to political, market, currency and regulatory risks or economic developments. International investments involve special risks that may in particular cause a loss in principal, including currency fluctuation, lower liquidity, different accounting methods and economic and political systems, and higher transaction costs.

These risks typically are greater in emerging markets. Securities of small‐ and medium‐sized companies tend to have a shorter history of operations, be more volatile and less liquid. Value stocks can perform differently from the market as a whole and other types of stocks. The material is provided for informational and/or educational purposes only and is not intended to be and should not be construed as investment, legal or tax advice and/or a legal opinion. Investors should consult their financial and tax adviser before making investments.

The opinions referenced are as of the date of publication, may be modified due to changes in the market or economic conditions, and may not necessarily come to pass.

Aristotle Capital Boston, LLC is an independent investment adviser registered under the Investment Advisers Act of 1940, as amended. Registration does not imply a certain level of skill or training. More information about Aristotle Boston, including our investment strategies, fees and objectives, can be found in our Form ADV Part 2, which is available upon request. ACB-2407-11

Performance Disclosures

Sources: CAPS Composite Hub, Russell Investments

Composite returns for periods ended June 30, 2024, are preliminary pending final account reconciliation.

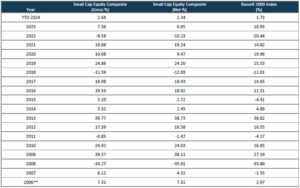

*The Aristotle Small Cap Equity Composite has an inception date of November 1, 2006 at a predecessor firm. During this time, Jack McPherson and Dave Adams had primary responsibility for managing the strategy. Performance starting January 1, 2015 was achieved at Aristotle Boston.

**For the period November 2006 through December 2006.

Past performance is not indicative of future results. Performance results for periods greater than one year have been annualized.

Effective January 1, 2022, the Aristotle Small Cap Equity Composite has been redefined to exclude accounts with meaningful industry-specific restrictions or substantial values-based screens hampering implementation of the small cap strategy.

Returns are presented gross and net of investment advisory fees and include the reinvestment of all income. Gross returns will be reduced by fees and other expenses that may be incurred in the management of the account. Net returns are presented net of actual investment advisory fees and after the deduction of all trading expenses. Please see important disclosures enclosed within this document.

Index Disclosures

The Russell 2000® Index measures the performance of the small cap segment of the U.S. equity universe. The Russell 2000 Index is a subset of the Russell 3000® Index representing approximately 10% of the total market capitalization of that index. It includes approximately 2000 of the smallest securities based on a combination of their market cap and current index membership. The Russell 2000 Growth® Index measures the performance of the small cap companies located in the United States that also exhibit a growth probability. The Russell 2000 Value® Index measures the performance of the small cap companies located in the United States that also exhibit a value probability. The Russell 1000® Index measures the performance of the large cap segment of the U.S. equity universe. The Russell 1000 Index is a subset of the Russell 3000® Index, representing approximately 90% of the total market capitalization of that index. It includes approximately 1,000 of the largest securities based on a combination of their market capitalization and current index membership. The volatility (beta) of the composite may be greater or less than the benchmarks. It is not possible to invest directly in these indices. The Consumer Price Index (CPI) is a measure of the average change over time in the prices paid by urban consumers for a market basket of consumer goods and services.

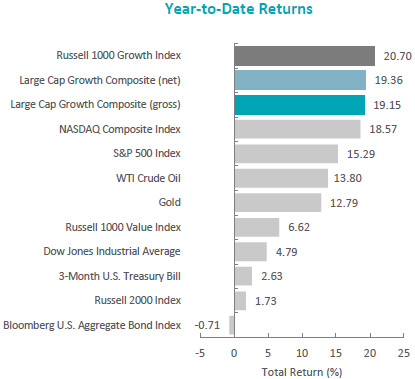

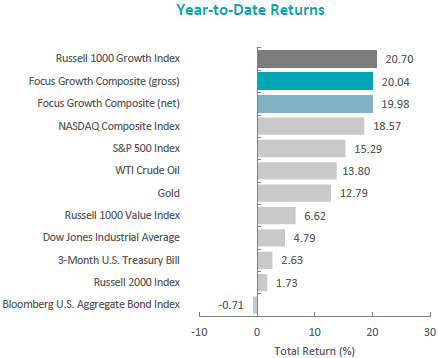

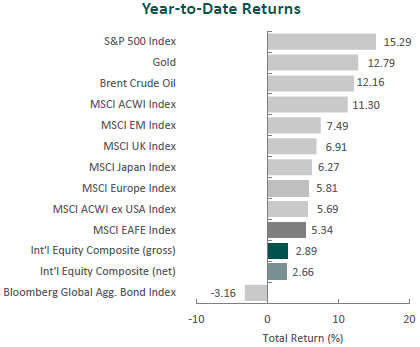

The U.S. equity market achieved record highs, as the S&P 500 Index rose 4.28% during the period. Gains were once again driven by the “Magnificent 7.” This narrow group of stocks was responsible for the majority of the S&P 500’s return during the quarter. Concurrently, the Bloomberg U.S. Aggregate Bond Index returned 0.07% for the quarter. In terms of style, the Russell 1000 Value Index underperformed its growth counterpart by 10.50%.

On a sector basis gains were made from seven of the eleven sectors within the Russell 1000 Growth index led by Information Technology and Communication Services. The worst performing sectors were Materials and Industrials.

Sources: CAPS CompositeHubTM, Bloomberg Past performance is not indicative of future results. Aristotle Atlantic Large Cap Growth Composite returns are presented gross and net of investment advisory fees and include the reinvestment of all income. Gross returns will be reduced by fees and other expenses that may be incurred in the management of the account. Net returns are presented net of actual investment advisory fees and after the deduction of all trading expenses. Aristotle Atlantic Composite returns are preliminary pending final account reconciliation. Please see important disclosures at the end of this document.

Data released during the period showed that U.S. economic growth slowed to an annual rate of 1.4% in the first quarter from 3.4% in the last quarter of 2023, as consumer spending, exports and government spending decelerated. Meanwhile, CPI inflation rose at an annual rate of 3.4% in April and 3.3% in May. This combination of sluggish economic growth and persistent inflation raised concerns about potential stagflation. However, the U.S. labor market remained strong, with unemployment at 4.0%, and consumer spending continued to grow.

Due to the unchanged macroeconomic landscape, with elevated inflation and a healthy labor market, the Federal Reserve (Fed) maintained the benchmark federal funds rate’s targeted range of 5.25% to 5.50% and continued reducing its holdings of Treasury securities. Fed Chair Powell emphasized patience in monetary policy changes and indicated it may take longer than expected to lower rates, as the committee is seeking greater confidence that inflation is sustainably moving toward its 2% target.

Corporate earnings were strong, with S&P 500 companies reporting earnings growth of 6.0% and more companies exceeding EPS estimates compared to the previous quarter. Despite slowing economic growth, fewer companies discussed the potential for a recession on earnings calls, and fewer companies mentioned inflation.

In geopolitics, tensions remained high as President Biden hiked tariffs on $18 billion of imports from China in a bid to protect U.S. workers and businesses. In the Middle East, the U.S. continued efforts to stabilize maritime traffic in the Red Sea while also facing criticism from Israeli Prime Minister Netanyahu, who claimed the U.S. was withholding weapons from Israel. The U.S. presidential campaign season also began in earnest, with the first debate between incumbent Joe Biden and Republican rival Donald Trump taking place in June.

Performance and Attribution Summary

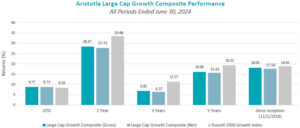

For the second quarter of 2024, Aristotle Atlantic’s Large Cap Growth Composite posted a total return of 8.77% gross of fees (8.71% net of fees), outperforming the 8.33% return of the Russell 1000 Growth Index.

Performance (%)

2Q24

1 Year

3 Years

5 Years

Since Inception*

Large Cap Growth Composite (gross)

8.77

28.37

6.81

16.08

18.05

Large Cap Growth Composite (net)

8.71

27.71

6.37

15.61

17.58

Russell 1000 Growth Index

8.33

33.48

11.27

19.32

19.43

*The Large Cap Growth Composite has an inception date of November 1, 2016. Past performance is not indicative of future results. Aristotle Atlantic Large Cap Growth Equity Composite returns are presented gross and net of investment advisory fees and include the reinvestment of all income. Gross returns will be reduced by fees and other expenses that may be incurred in the management of the account. Net returns are presented net of actual investment advisory fees and after the deduction of all trading expenses. Aristotle Atlantic Composite returns are preliminary pending final account reconciliation. Please see important disclosures at the end of this document.

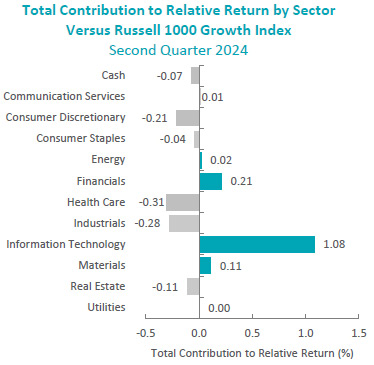

Sources: FactSet Past performance is not indicative of future results. Attribution results are based on sector returns which are gross of investment advisory fees. Attribution is based on performance that is gross of investment advisory fees and includes the reinvestment of income. Please see important disclosures at the end of this document.

During the second quarter, the portfolio’s outperformance relative to the Russell 1000 Growth Index was primarily due to security selection. Security selection in Information Technology and Financials contributed the most to relative performance. Conversely, security selection in Heath Care and Industrials detracted from relative performance.

Contributors and Detractors for 2Q 2024

Relative Contributors

Relative Detractors

Nvidia

Dexcom

KLA Corporation

Darling Ingredients

Guardant Health

Visa

Costco Wholesale

Expedia Group

Vertex Pharmaceuticals

Norfolk Southern

Contributors

Nvidia

Nvidia contributed to portfolio performance in the second quarter as investors continued to view positively the new product roadmap for the rest of the year. The company sees accelerating demand for its GPU semiconductors from hyperscalers and enterprises. Nvidia’s GPU semiconductors continue to be the industry-leading building blocks of the accelerated computing data center architecture to drive AI compute and applications.

KLA Corporation

KLA contributed to portfolio performance in the second quarter as the company reported a strong March quarter. The results were driven by better-than-expected performance in patterning and services segments. The company also provided positive commentary on customer orders and increased visibility on growing sequential revenue through the rest of 2024. Commentary surrounding wafer fab equipment (WFE) spending for 2024 shows improving demand, with 2024 at least flat versus 2023 and growing customer spend driven by strong foundry/logic and high bandwidth memory (HBM) demand from accelerating AI-compute infrastructure spend.

Detractors

Dexcom

Dexcom detracted from performance in the quarter as the stock price gave back all the strong gains from the first quarter of this year. The company reported strong first quarter earnings, beating consensus estimates for the top and bottom lines, highlighted by 25% organic revenue growth. Additionally, it raised the low end of full-year revenue guidance based on the strong start to the year, with record new patient starts. Dexcom is launching an over-the-counter continuous glucose monitoring device set to target the over 25 million Type 2 diabetes patients who are not dependent on insulin. Furthermore, the medical device company recently expanded its salesforce to better address the ~200K primary care physicians in the United States. We see several catalysts going forward, and the stock is trading at a discount to historical valuation metrics.

Darling Ingredients

Darling Ingredients detracted from portfolio performance in the quarter, as shares continued to be weak following an in-line quarterly earnings report where the company provided initial 2024 EBITDA guidance of $1.3B to $1.4B, below consensus estimates. On a positive note, the company called out improving fat prices exiting the first quarter. Additionally, in its renewable diesel joint venture, the company has worked through higher-cost feedstocks contracted during start-up, so renewable diesel margins should improve on the lower input prices. We believe there are several catalysts for Darling going forward, including the blenders tax credit transitioning to a producer’s tax credit on January 1, 2025 and positive commentary around contracting sustainable aviation fuel (SAF) at a $1-$2 per gallon premium to renewable diesel. SAF production starts were pulled forward to the fourth quarter from prior guidance of early 2025.

Recent Portfolio Activity

The table below shows all buys and sells completed during the quarter, followed by a brief rationale.

Buys

Sells

Analog Devices

ON Semiconductor

Broadcom

Buys

Analog Devices

Analog Devices is a global semiconductor leader dedicated to solving customers’ most complex engineering challenges. The company delivers innovations that connect technology to human breakthroughs and play a critical role at the intersection of the physical and digital worlds by providing the building blocks to sense, measure, interpret, connect and power. Analog designs, manufactures, tests and markets a broad portfolio of solutions, including integrated circuits, software and subsystems that leverage high-performance analog, mixed-signal and digital signal processing technologies. Its comprehensive product portfolio, deep domain expertise and advanced manufacturing capabilities extend across high-performance precision and high-speed mixed-signal, power management and processing technologies, including data converters, amplifiers, power management, radio frequency, integrated circuits, edge processors and other sensors. The company’s customers include original equipment manufacturers and customers that build electronic subsystems for integration into larger systems.

We see the company’s analog products providing exposure to high-growth trends, including automotive electrification and driver assistance systems, factory intelligence and automation, the Intelligent Edge, Internet of Things device proliferation, and sustainable energy. We expect the company to return excess free cash flow, benefiting shareholders.

Broadcom

Broadcom is a global technology leader that designs, develops and supplies a broad range of semiconductor and infrastructure software solutions. The company strategically focuses its research and development resources to address niche opportunities in target markets and leverage its extensive portfolio of U.S. and other patents and other intellectual property to integrate multiple technologies and create system-on-chip component and software solutions that target growth opportunities. Broadcom designs products and software that deliver high performance and provide mission-critical functionality. The company has a history of innovation in the semiconductor industry and offers thousands of products that are used in end products such as enterprise and data center networking, home connectivity, “set-top boxes broadband access”, telecommunication equipment, smartphones and base stations, data center servers and storage systems, factory automation, power generation and alternative energy systems, and electronic displays. Broadcom differentiates itself through its high-performance design and integration capabilities and focuses on developing products for target markets where it believes it can earn attractive margins.

We view Broadcom’s semiconductor business as being very well positioned to benefit from secular growth in data center networking, which is being driven by AI and cloud computing. The company continues to invest in research and development, and we see this as a competitive advantage for the company. Broadcom’s infrastructure software business is a recurring revenue business model that provides mission-critical mainframe support software to its customer base. The recent VMware acquisition will enhance this business strategy and accelerate the growth rate of this business unit, as VMware’s product suite includes key tools for AI server upgrades. Our long-term investment thesis is supported by Broadcom’s success in its strategy of maintaining technology and market share leadership in mission-critical markets with high switching costs and deep profit pools.

Sells

ON Semiconductor

We sold ON Semiconductor and have become more cautious on the global automotive market, especially for electric vehicles, which we believe will see a period of slower sales due to both new infrastructure requirements and consumers becoming more knowledgeable about the potential costs and issues with owning EVs. In addition, the market is becoming a lot more competitive on the supply side, with many new models being launched simultaneously, which we believe will lead to pricing pressures for the OEMs, which could create pricing headwinds for suppliers such as ON Semiconductor. While we see global EV penetration as continuing to increase over the next decade, supported by government incentives, we remain cautious in the near term and believe we are entering a period of lower sales trends following the explosive growth of the past three years.

Outlook

The equity markets in the second quarter posted positive returns, led by the broadening secular trend in AI. The move in interest rates was muted in the quarter as markets await a clear signal from the Federal Reserve on the timing of a rate reduction. On the margin, economic activity slowed, with multiple ISM manufacturing readings in contraction territory and a weakening housing market. Equity valuations remain high, with AI-focused companies contributing the most to these elevated levels. The geopolitical situation remains very unsettled, and a U.S. presidential election moves into focus, adding to the level of uncertainty. With many issues unresolved, we could see markets move into a period of higher volatility off very low levels. The equity markets continue to reflect the positive backdrop of growing earnings and a potential lowering of interest rates. Our focus will continue to be at the company level, with an emphasis on seeking to invest in companies with secular tailwinds or strong product-driven cycles.

Disclosures

The opinions expressed herein are those of Aristotle Atlantic Partners, LLC (Aristotle Atlantic) and are subject to change without notice. Past performance is not a guarantee or indicator of future results. This material is not financial advice or an offer to purchase or sell any product. You should not assume that any of the securities transactions, sectors or holdings discussed in this report were or will be profitable, or that recommendations Aristotle Atlantic makes in the future will be profitable or equal the performance of the securities listed in this report. The portfolio characteristics shown relate to the Aristotle Atlantic Large Cap Growth strategy. Not every client’s account will have these characteristics. Aristotle Atlantic reserves the right to modify its current investment strategies and techniques based on changing market dynamics or client needs. There is no assurance that any securities discussed herein will remain in an account’s portfolio at the time you receive this report or that securities sold have not been repurchased. The securities discussed may not represent an account’s entire portfolio and, in the aggregate, may represent only a small percentage of an account’s portfolio holdings. The performance attribution presented is of a representative account from Aristotle Atlantic’s Large Cap Growth Composite. The representative account is a discretionary client account which was chosen to most closely reflect the investment style of the strategy. The criteria used for representative account selection is based on the account’s period of time under management and its similarity of holdings in relation to the strategy. Recommendations made in the last 12 months are available upon request. Returns are presented gross and net of investment advisory fees and include the reinvestment of all income. Gross returns will be reduced by fees and other expenses that may be incurred in the management of the account. Net returns are presented net of actual investment advisory fees and after the deduction of all trading expenses.

All investments carry a certain degree of risk, including the possible loss of principal. Investments are also subject to political, market, currency and regulatory risks or economic developments. International investments involve special risks that may in particular cause a loss in principal, including currency fluctuation, lower liquidity, different accounting methods and economic and political systems, and higher transaction costs. These risks typically are greater in emerging markets. Securities of small‐ and medium‐sized companies tend to have a shorter history of operations, be more volatile and less liquid. Value stocks can perform differently from the market as a whole and other types of stocks.

The material is provided for informational and/or educational purposes only and is not intended to be and should not be construed as investment, legal or tax advice and/or a legal opinion. Investors should consult their financial and tax adviser before making investments. The opinions referenced are as of the date of publication, may be modified due to changes in the market or economic conditions, and may not necessarily come to pass. Information and data presented has been developed internally and/or obtained from sources believed to be reliable. Aristotle Atlantic does not guarantee the accuracy, adequacy or completeness of such information.

Aristotle Atlantic Partners, LLC is an independent registered investment adviser under the Advisers Act of 1940, as amended. Registration does not imply a certain level of skill or training. More information about Aristotle Atlantic, including our investment strategies, fees and objectives, can be found in our Form ADV Part 2, which is available upon request. AAP-2407-12

Performance Disclosure

Sources: CAPS CompositeHubTM, Russell Investments

Composite returns for all periods ended June 30, 2024 are preliminary pending final account reconciliation.

Past performance is not indicative of future results. Performance results for periods greater than one year have been annualized. Returns are presented gross and net of investment advisory fees and include the reinvestment of all income. Gross returns will be reduced by fees and other expenses that may be incurred in the management of the account. Net returns are presented net of actual investment advisory fees and after the deduction of all trading expenses.

Index Disclosure

The Russell 1000® Growth Index measures the performance of the large cap growth segment of the U.S. equity universe. It includes those Russell 1000 companies with higher price-to-book ratios and higher forecasted growth values. This index has been selected as the benchmark and is used for comparison purposes only. The Russell 1000® Value Index measures the performance of the large cap value segment of the U.S. equity universe. It includes those Russell 1000 companies with lower price-to-book ratios and lower expected growth values. The Russell 2000®Index measures the performance of the small cap segment of the U.S. equity universe. The Russell 2000 Index is a subset of the Russell 3000® Index representing approximately 10% of the total market capitalization of that index. It includes approximately 2000 of the smallest securities based on a combination of their market cap and current index membership. The S&P 500® Index is the Standard & Poor’s Composite Index of 500 stocks and is a widely recognized, unmanaged index of common stock prices. The Dow Jones Industrial Average® is a price-weighted measure of 30 U.S. blue-chip companies. The Index covers all industries except transportation and utilities. The NASDAQ Composite Index measures all NASDAQ domestic and international based common type stocks listed on The NASDAQ Stock Market. The NASDAQ Composite includes over 3,000 companies, more than most other stock market indices. The Bloomberg U.S. Aggregate Bond Index is an unmanaged index of domestic investment grade bonds, including corporate, government and mortgage-backed securities. The WTI Crude Oil Index is a major trading classification of sweet light crude oil that serves as a major benchmark price for oil consumed in the United States. The 3-Month U.S. Treasury Bill is a short-term debt obligation backed by the U.S. Treasury Department with a maturity of three months. The Consumer Price Index (CPI) is a measure of the average change over time in the prices paid by urban consumers for a market basket of consumer goods and services. While stock selection is not governed by quantitative rules, a stock typically is added only if the company has an excellent reputation, demonstrates sustained growth and is of interest to a large number of investors. The volatility (beta) of the Composite may be greater or less than its respective benchmarks. It is not possible to invest directly in these indices.

The U.S. equity market achieved record highs, as the S&P 500 Index rose 4.28% during the period. Gains were once again driven by the “Magnificent 7.” This narrow group of stocks was responsible for the majority of the S&P 500’s return during the quarter. Concurrently, the Bloomberg U.S. Aggregate Bond Index returned 0.07% for the quarter. In terms of style, the Russell 1000 Value Index underperformed its growth counterpart by 10.50%.

Sources: CAPS CompositeHubTM, Bloomberg Past performance is not indicative of future results. Aristotle Atlantic Focus Growth Composite returns are presented gross and net of investment advisory fees and include the reinvestment of all income. Gross returns will be reduced by fees and other expenses that may be incurred in the management of the account. Net returns are presented net of actual investment advisory fees and after the deduction of all trading expenses. Aristotle Atlantic Composite returns are preliminary pending final account reconciliation. Please see important disclosures at the end of this document.

On a sector basis gains were made from seven of the eleven sectors within the Russell 1000 Growth index led by Information Technology and Communication Services. The worst performing sectors were Materials and Industrials.

Data released during the period showed that U.S. economic growth slowed to an annual rate of 1.4% in the first quarter from 3.4% in the last quarter of 2023, as consumer spending, exports and government spending decelerated. Meanwhile, CPI inflation rose at an annual rate of 3.4% in April and 3.3% in May. This combination of sluggish economic growth and persistent inflation raised concerns about potential stagflation. However, the U.S. labor market remained strong, with unemployment at 4.0%, and consumer spending continued to grow.

Due to the unchanged macroeconomic landscape, with elevated inflation and a healthy labor market, the Federal Reserve (Fed) maintained the benchmark federal funds rate’s targeted range of 5.25% to 5.50% and continued reducing its holdings of Treasury securities. Fed Chair Powell emphasized patience in monetary policy changes and indicated it may take longer than expected to lower rates, as the committee is seeking greater confidence that inflation is sustainably moving toward its 2% target.

Corporate earnings were strong, with S&P 500 companies reporting earnings growth of 6.0% and more companies exceeding EPS estimates compared to the previous quarter. Despite slowing economic growth, fewer companies discussed the potential for a recession on earnings calls, and fewer companies mentioned inflation.

In geopolitics, tensions remained high as President Biden hiked tariffs on $18 billion of imports from China in a bid to protect U.S. workers and businesses. In the Middle East, the U.S. continued efforts to stabilize maritime traffic in the Red Sea while also facing criticism from Israeli Prime Minister Netanyahu, who claimed the U.S. was withholding weapons from Israel. The U.S. presidential campaign season also began in earnest, with the first debate between incumbent Joe Biden and Republican rival Donald Trump taking place in June.

Performance and Attribution Summary

For the second quarter of 2024, Aristotle Atlantic’s Focus Growth Composite posted a total return of 8.71% gross of fees (8.68% net of fees), outperforming the 8.33% total return of the Russell 1000 Growth Index.

Performance (%)

2Q24

1 Year

3 Years

5 Years

Since Inception*

Focus Growth Composite (gross)

8.71

30.46

5.96

15.09

14.74

Focus Growth Composite (net)

8.68

30.34

5.86

14.94

14.50

Russell 1000 Growth Index

8.33

33.48

11.27

19.32

17.49

*The Focus Growth Composite has an inception date of March 1, 2018. Past performance is not indicative of future results. Aristotle Atlantic Focus Growth Composite returns are presented gross and net of investment advisory fees and include the reinvestment of all income. Gross returns will be reduced by fees and other expenses that may be incurred in the management of the account. Net returns are presented net of actual investment advisory fees and after the deduction of all trading expenses. Aristotle Atlantic Composite returns are preliminary pending final account reconciliation. Please see important disclosures at the end of this document.

Sources: FactSet Past performance is not indicative of future results. Attribution results are based on sector returns which are gross of investment advisory fees. Attribution is based on performance that is gross of investment advisory fees and includes the reinvestment of income. Please see important disclosures at the end of this document.

During the second quarter, the portfolio’s outperformance relative to the Russell 1000 Growth Index was due to allocation effects and security selection. Security selection in Information Technology contributed the most to relative performance. Conversely, security selection in Health Care detracted from relative performance.

Contributors and Detractors for 2Q 2024

Relative Contributors

Relative Detractors

Nvidia

Visa

KLA Corporation

Dexcom

Guardant Health

Darling Ingredients

Costco Wholesale

Prologis

Netflix

Norfolk Southern

Contributors

Nvidia

Nvidia contributed to portfolio performance in the second quarter as investors continued to view positively the new product roadmap for the rest of the year. The company sees accelerating demand for its GPU semiconductors from hyperscalers and enterprises. Nvidia’s GPU semiconductors continue to be the industry-leading building blocks of the accelerated computing data center architecture to drive AI compute and applications.

KLA Corporation

KLA contributed to portfolio performance in the second quarter as the company reported a strong March quarter. The results were driven by better-than-expected performance in patterning and services segments. The company also provided positive commentary on customer orders and increased visibility on growing sequential revenue through the rest of 2024. Commentary surrounding wafer fab equipment (WFE) spending for 2024 shows improving demand, with 2024 at least flat versus 2023 and growing customer spend driven by strong foundry/logic and high bandwidth memory (HBM) demand from accelerating AI-compute infrastructure spend.

Detractors

Visa

Visa detracted from portfolio performance in the second quarter despite a solid earnings report early in the quarter that highlighted continued growth in payment volumes and value-added services. However, shares declined late in the quarter due to a court denying a proposed settlement that would have ended interchange fee-related litigation between Visa, Mastercard and merchant plaintiffs. As a result, uncertainty surrounding the possible outcomes of the litigation has created an overhang for Visa’s shares, even though interchange fees are charged by card-issuing financial institutions, not networks like Visa and Mastercard.

Dexcom

Dexcom detracted from performance in the quarter as the stock price gave back all the strong gains from the first quarter of this year. The company reported strong first quarter earnings, beating consensus estimates for the top and bottom lines, highlighted by 25% organic revenue growth. Additionally, it raised the low end of full-year revenue guidance based on the strong start to the year, with record new patient starts. Dexcom is launching an over-the-counter continuous glucose monitoring device set to target the over 25 million Type 2 diabetes patients who are not dependent on insulin. Furthermore, the medical device company recently expanded its salesforce to better address the ~200K primary care physicians in the United States. We see several catalysts going forward, and the stock is trading at a discount to historical valuation metrics.

Recent Portfolio Activity

The table below shows all buys and sells completed during the quarter, followed by a brief rationale.

Buys

Sells

Analog Devices

ON Semiconductor

Broadcom

Buys

Analog Devices

Analog Devices is a global semiconductor leader dedicated to solving customers’ most complex engineering challenges. The company delivers innovations that connect technology to human breakthroughs and play a critical role at the intersection of the physical and digital worlds by providing the building blocks to sense, measure, interpret, connect and power. Analog designs, manufactures, tests and markets a broad portfolio of solutions, including integrated circuits, software and subsystems that leverage high-performance analog, mixed-signal and digital signal processing technologies. Its comprehensive product portfolio, deep domain expertise and advanced manufacturing capabilities extend across high-performance precision and high-speed mixed-signal, power management and processing technologies, including data converters, amplifiers, power management, radio frequency, integrated circuits, edge processors and other sensors. The company’s customers include original equipment manufacturers and customers that build electronic subsystems for integration into larger systems.

We see the company’s analog products providing exposure to high-growth trends, including automotive electrification and driver assistance systems, factory intelligence and automation, the Intelligent Edge, Internet of Things device proliferation, and sustainable energy. We expect the company to return excess free cash flow, benefiting shareholders.

Broadcom

Broadcom is a global technology leader that designs, develops and supplies a broad range of semiconductor and infrastructure software solutions. The company strategically focuses its research and development resources to address niche opportunities in target markets and leverage its extensive portfolio of U.S. and other patents and other intellectual property to integrate multiple technologies and create system-on-chip component and software solutions that target growth opportunities. Broadcom designs products and software that deliver high performance and provide mission-critical functionality. The company has a history of innovation in the semiconductor industry and offers thousands of products that are used in end products such as enterprise and data center networking, home connectivity, “set-top boxes broadband access”, telecommunication equipment, smartphones and base stations, data center servers and storage systems, factory automation, power generation and alternative energy systems, and electronic displays. Broadcom differentiates itself through its high-performance design and integration capabilities and focuses on developing products for target markets where it believes it can earn attractive margins.

We view Broadcom’s semiconductor business as being very well positioned to benefit from secular growth in data center networking, which is being driven by AI and cloud computing. The company continues to invest in research and development, and we see this as a competitive advantage for the company. Broadcom’s infrastructure software business is a recurring revenue business model that provides mission-critical mainframe support software to its customer base. The recent VMware acquisition will enhance this business strategy and accelerate the growth rate of this business unit, as VMware’s product suite includes key tools for AI server upgrades. Our long-term investment thesis is supported by Broadcom’s success in its strategy of maintaining technology and market share leadership in mission-critical markets with high switching costs and deep profit pools.

Sells

ON Semiconductor

We sold ON Semiconductor and have become more cautious on the global automotive market, especially for electric vehicles, which we believe will see a period of slower sales due to both new infrastructure requirements and consumers becoming more knowledgeable about the potential costs and issues with owning EVs. In addition, the market is becoming a lot more competitive on the supply side, with many new models being launched simultaneously, which we believe will lead to pricing pressures for the OEMs, which could create pricing headwinds for suppliers such as ON Semiconductor. While we see global EV penetration as continuing to increase over the next decade, supported by government incentives, we remain cautious in the near term and believe we are entering a period of lower sales trends following the explosive growth of the past three years.

Outlook

The equity markets in the second quarter posted positive returns, led by the broadening secular trend in AI. The move in interest rates was muted in the quarter as markets await a clear signal from the Federal Reserve on the timing of a rate reduction. On the margin, economic activity slowed, with multiple ISM manufacturing readings in contraction territory and a weakening housing market. Equity valuations remain high, with AI-focused companies contributing the most to these elevated levels. The geopolitical situation remains very unsettled, and a U.S. presidential election moves into focus, adding to the level of uncertainty. With many issues unresolved, we could see markets move into a period of higher volatility off very low levels. The equity markets continue to reflect the positive backdrop of growing earnings and a potential lowering of interest rates. Our focus will continue to be at the company level, with an emphasis on seeking to invest in companies with secular tailwinds or strong product-driven cycles.

Disclosures

The opinions expressed herein are those of Aristotle Atlantic Partners, LLC (Aristotle Atlantic) and are subject to change without notice. Past performance is not a guarantee or indicator of future results. This material is not financial advice or an offer to purchase or sell any product. You should not assume that any of the securities transactions, sectors or holdings discussed in this report were or will be profitable, or that recommendations Aristotle Atlantic makes in the future will be profitable or equal the performance of the listed in this report. The portfolio characteristics shown relate to the Aristotle Atlantic Focus Growth strategy. Not every client’s account will have these characteristics. Aristotle Atlantic reserves the right to modify its current investment strategies and techniques based on changing market dynamics or client needs. There is no assurance that any securities discussed herein will remain in an account’s portfolio at the time you receive this report or that securities sold have not been repurchased. The securities discussed may not represent an account’s entire portfolio and, in the aggregate, may represent only a small percentage of an account’s portfolio holdings. The performance attribution presented is of a representative account from Aristotle Atlantic’s Focus Growth Composite. The representative account is a discretionary client account which was chosen to most closely reflect the investment style of the strategy. The criteria used for representative account selection is based on the account’s period of time under management and its similarity of holdings in relation to the strategy. Recommendations made in the last 12 months are available upon request. Returns are presented gross and net of investment advisory fees and include the reinvestment of all income. Gross returns will be reduced by fees and other expenses that may be incurred in the management of the account. Net returns are presented net of actual investment advisory fees and after the deduction of all trading expenses.

All investments carry a certain degree of risk, including the possible loss of principal. Investments are also subject to political, market, currency and regulatory risks or economic developments. International investments involve special risks that may in particular cause a loss in principal, including currency fluctuation, lower liquidity, different accounting methods and economic and political systems, and higher transaction costs. These risks typically are greater in emerging markets. Securities of small‐ and medium‐sized companies tend to have a shorter history of operations, be more volatile and less liquid. Value stocks can perform differently from the market as a whole and other types of stocks.

The material is provided for informational and/or educational purposes only and is not intended to be and should not be construed as investment, legal or tax advice and/or a legal opinion. Investors should consult their financial and tax adviser before making investments. The opinions referenced are as of the date of publication, may be modified due to changes in the market or economic conditions, and may not necessarily come to pass. Information and data presented has been developed internally and/or obtained from sources believed to be reliable. Aristotle Atlantic does not guarantee the accuracy, adequacy or completeness of such information.

Aristotle Atlantic Partners, LLC is an independent registered investment adviser under the Advisers Act of 1940, as amended. Registration does not imply a certain level of skill or training. More information about Aristotle Atlantic, including our investment strategies, fees and objectives, can be found in our Form ADV Part 2, which is available upon request. AAP-2407-11

Performance Disclosures

Sources: CAPS CompositeHubTM, Russell Investments

Composite returns for all periods ended June 30, 2024 are preliminary pending final account reconciliation.

Past performance is not indicative of future results. Performance results for periods greater than one year have been annualized. Returns are presented gross and net of investment advisory fees and include the reinvestment of all income. Gross returns will be reduced by fees and other expenses that may be incurred in the management of the account. Net returns are presented net of actual investment advisory fees and after the deduction of all trading expenses.

Index Disclosures

The Russell 1000® Growth Index measures the performance of the large cap growth segment of the U.S. equity universe. It includes those Russell 1000 companies with higher price-to-book ratios and higher forecasted growth values. This index has been selected as the benchmark and is used for comparison purposes only. The Russell 1000® Value Index measures the performance of the large cap value segment of the U.S. equity universe. It includes those Russell 1000 companies with lower price-to-book ratios and lower expected growth values. The S&P 500® Index is the Standard & Poor’s Composite Index of 500 stocks and is a widely recognized, unmanaged index of common stock prices. The Russell 2000® Index measures the performance of the small cap segment of the U.S. equity universe. The Russell 2000 Index is a subset of the Russell 3000® Index representing approximately 10% of the total market capitalization of that index. It includes approximately 2,000 of the smallest securities based on a combination of their market cap and current index membership. The Dow Jones Industrial Average® is a price-weighted measure of 30 U.S. blue-chip companies. The Index covers all industries except transportation and utilities. The NASDAQ Composite Index measures all NASDAQ domestic and international based common type stocks listed on The NASDAQ Stock Market. The NASDAQ Composite includes over 3,000 companies, more than most other stock market indices. The Bloomberg U.S. Aggregate Bond Index is an unmanaged index of domestic investment grade bonds, including corporate, government and mortgage-backed securities. The WTI Crude Oil Index is a major trading classification of sweet light crude oil that serves as a major benchmark price for oil consumed in the United States. The 3-Month U.S. Treasury Bill is a short-term debt obligation backed by the U.S. Treasury Department with a maturity of three months. The Consumer Price Index (CPI) is a measure of the average change over time in the prices paid by urban consumers for a market basket of consumer goods and services. While stock selection is not governed by quantitative rules, a stock typically is added only if the company has an excellent reputation, demonstrates sustained growth and is of interest to a large number of investors. The volatility (beta) of the Composite may be greater or less than its respective benchmarks. It is not possible to invest directly in these indices.

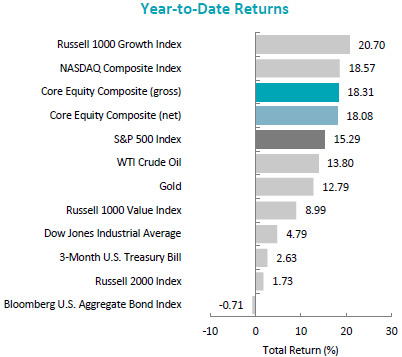

The U.S. equity market achieved record highs, as the S&P 500 Index rose 4.28% during the period. Gains were once again driven by the “Magnificent 7.” This narrow group of stocks was responsible for the majority of the S&P 500’s return during the quarter. Concurrently, the Bloomberg U.S. Aggregate Bond Index returned 0.07% for the quarter. In terms of style, the Russell 1000 Value Index underperformed its growth counterpart by 10.50%.

On a sector basis gains were made from five of the eleven sectors within the S&P 500 index led by Information Technology and Communication Services. The worst performing sectors were Materials and Industrials.

Sources: CAPS CompositeHubTM, Bloomberg Past performance is not indicative of future results. Aristotle Atlantic Core Equity Composite returns are presented gross and net of investment advisory fees and include the reinvestment of all income. Gross returns will be reduced by fees and other expenses that may be incurred in the management of the account. Net returns are presented net of actual investment advisory fees and after the deduction of all trading expenses. Aristotle Atlantic Composite returns are preliminary pending final account reconciliation. Please see important disclosures at the end of this document.

Data released during the period showed that U.S. economic growth slowed to an annual rate of 1.4% in the first quarter from 3.4% in the last quarter of 2023, as consumer spending, exports and government spending decelerated. Meanwhile, CPI inflation rose at an annual rate of 3.4% in April and 3.3% in May. This combination of sluggish economic growth and persistent inflation raised concerns about potential stagflation. However, the U.S. labor market remained strong, with unemployment at 4.0%, and consumer spending continued to grow.

Due to the unchanged macroeconomic landscape, with elevated inflation and a healthy labor market, the Federal Reserve (Fed) maintained the benchmark federal funds rate’s targeted range of 5.25% to 5.50% and continued reducing its holdings of Treasury securities. Fed Chair Powell emphasized patience in monetary policy changes and indicated it may take longer than expected to lower rates, as the committee is seeking greater confidence that inflation is sustainably moving toward its 2% target.

Corporate earnings were strong, with S&P 500 companies reporting earnings growth of 6.0% and more companies exceeding EPS estimates compared to the previous quarter. Despite slowing economic growth, fewer companies discussed the potential for a recession on earnings calls, and fewer companies mentioned inflation.

In geopolitics, tensions remained high as President Biden hiked tariffs on $18 billion of imports from China in a bid to protect U.S. workers and businesses. In the Middle East, the U.S. continued efforts to stabilize maritime traffic in the Red Sea while also facing criticism from Israeli Prime Minister Netanyahu, who claimed the U.S. was withholding weapons from Israel. The U.S. presidential campaign season also began in earnest, with the first debate between incumbent Joe Biden and Republican rival Donald Trump taking place in June.

Performance and Attribution Summary

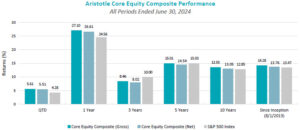

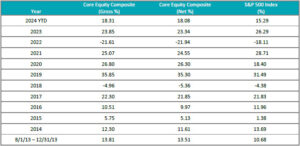

For the second quarter of 2024, Aristotle Atlantic’s Core Equity Composite posted a total return of 5.61% gross of fees (5.51% net of fees), outperforming the S&P 500 Index, which recorded a total return of 4.28%.

Performance (%)

2Q24

1 Year

3 Years

5 Years

10 Years

Since Inception*

Core Equity Composite (gross)

5.61

27.10

8.46

15.01

13.55

14.28

Core Equity Composite (net)

5.51

26.61

8.02

14.54

13.05

13.76

S&P 500 Index

4.28

24.56

10.00

15.03

12.85

13.47

*The Core Equity Composite has an inception date of August 1, 2013. Past performance is not indicative of future results. Aristotle Atlantic Core Equity Composite returns are presented gross and net of investment advisory fees and include the reinvestment of all income. Gross returns will be reduced by fees and other expenses that may be incurred in the management of the account. Net returns are presented net of actual investment advisory fees and after the deduction of all trading expenses. Aristotle Atlantic Composite returns are preliminary pending final account reconciliation. Please see important disclosures at the end of this document.

Source: FactSet Past performance is not indicative of future results. Attribution results are based on sector returns which are gross of investment advisory fees. Attribution is based on performance that is gross of investment advisory fees and includes the reinvestment of income. Please see important disclosures at the end of this document.

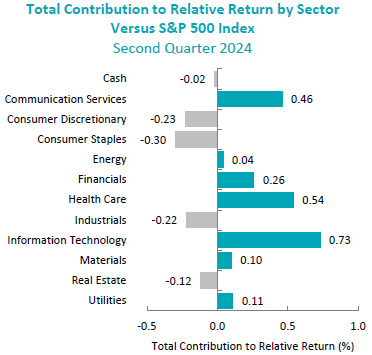

During the second quarter, the portfolio’s outperformance relative to the S&P 500 Index was primarily due to security selection. Security selection in Information Technology and Health Care contributed the most to relative performance. Conversely, security selection in Consumer Staples and Consumer Discretionary detracted from relative performance.

Contributors and Detractors for 2Q 2024

Relative Contributors

Relative Detractors

Nvidia

Darling Ingredients

Alphabet

Norfolk Southern

Broadcom

Halliburton

Guardant Health

AMETEK

Costco Wholesale

Estée Lauder

Contributors

Nvidia

Nvidia contributed to portfolio performance in the second quarter as investors continued to view positively the new product roadmap for the rest of the year. The company sees accelerating demand for its GPU semiconductors from hyperscalers and enterprises. Nvidia’s GPU semiconductors continue to be the industry-leading building blocks of the accelerated computing data center architecture to drive AI compute and applications.

Alphabet

Alphabet contributed to portfolio performance in the second quarter, boosted by a strong earnings report featuring better-than-expected revenues across all businesses. The company’s positive commentary on the long-term monetization of its AI investments, dividend initiation and increase in its share buyback program contributed to the strong performance. Additionally, evidence increasingly suggests that competitors’ GenAI use cases have not disrupted Alphabet’s search business, allowing the company to maintain its market leadership and attract incremental advertising dollars.

Detractors

Darling Ingredients

Darling Ingredients detracted from portfolio performance in the quarter, as shares continued to be weak following an in-line quarterly earnings report where the company provided initial 2024 EBITDA guidance of $1.3B to $1.4B, below consensus estimates. On a positive note, the company called out improving fat prices exiting the first quarter. Additionally, in its renewable diesel joint venture, the company has worked through higher-cost feedstocks contracted during start-up, so renewable diesel margins should improve on the lower input prices. We believe there are several catalysts for Darling going forward, including the blenders tax credit transitioning to a producer’s tax credit on January 1, 2025 and positive commentary around contracting sustainable aviation fuel (SAF) at a $1-$2 per gallon premium to renewable diesel. SAF production starts were pulled forward to the fourth quarter from prior guidance of early 2025.

Norfolk Southern

Norfolk Southern detracted from performance in the second quarter. The company reported a worse-than-expected earnings result for its first quarter in late April. In the second quarter, the company has been reporting weaker-than-expected railcar volumes on its network. This weaker volume has resulted in some sell-side analysts reducing their estimates for the second quarter of 2024. In addition, sentiment is weak because an activist shareholder was not successful in replacing the CEO of Norfolk Southern during a proxy battle in May; however, the activist did succeed in replacing some board members.

Recent Portfolio Activity

The table below shows all buys and sells completed during the quarter.

Buys

Sells

Amphenol

Abbott Laboratories

Boston Scientific

Accenture

Microchip Technology

Teleflex

Buys

Amphenol

Amphenol is one of the world’s largest designers, manufacturers and marketers of electrical, electronic and fiber optic connectors and interconnect systems; antennas; sensors and sensor-based products; and coaxial and high-speed specialty cable. The company estimates, based on recent reports of industry analysts, that worldwide sales of interconnect and sensor-related products were approximately $235 billion in 2023. The company aligns its businesses into three reportable business segments: Harsh Environment Solutions, Communications Solutions, and Interconnect and Sensor Systems. The company sells products to customers in a diversified set of end markets.

We see Amphenol benefiting from increased spending by cloud service providers, hyperscalers and enterprises on new data center architectures that enable AI computing technologies. The increased interconnect content that AI-enabled data centers require, we believe, will underpin a double-digit sales growth outlook for the company over the next few years. The company has attractive end-market diversification, with exposure to both short-cycle and long-cycle, and no single end market vertical represents more than 25% of revenues. Additionally, Amphenol has strong free cash flow generation, which has supported a successful M&A strategy that has driven enhanced advancement.

Boston Scientific

Boston Scientific is a global developer, manufacturer and marketer of medical devices that are used in a broad range of interventional medical specialties. The company develops cardiovascular and cardiac rhythm management products, including imaging catheters, imaging systems and guidewires. It also makes devices used for electrophysiology, endoscopy, pain management (neuromodulation), urology and pelvic health, including laser systems, hydrogel systems and brain stimulation systems. Boston Scientific markets its products in about 130 countries; the U.S. generates about 60% of revenue.

We believe Boston Scientific, as a leader in medical devices, is benefiting from the strong utilization trends coming out of COVID, positive demographic trends with aging patients, and new product innovation to gain market share. The company has executed well against the long-range plan issued last fall, which calls for organic sales growth in the range of 8%-10%, 150 basis points of operating margin expansion and category leadership over the period 2024 through 2026. Additionally, we see a consistent track record of accelerating organic sales growth and a track record of accretive M&A.

Microchip Technology

Microchip develops, manufactures and sells smart, connected and secure embedded control solutions used by its customers for a wide variety of applications. With over 30 years of technology leadership, Microchip’s broad product portfolio is a Total System Solution for its customers that can provide a large portion of the silicon requirements in their applications. Total System Solution is a combination of hardware, software and services that helps customers increase their revenue, reduce their costs and manage their risks compared to other solutions. Microchip’s synergistic product portfolio empowers disruptive growth trends, including 5G, data centers, sustainability, Internet of Things and edge computing, advanced driver assist systems and autonomous driving, and electric vehicles in key end markets such as automotive, aerospace and defense, communications, consumer appliances, data centers and computing, and industrial.

We believe Microchip’s Total System Solution will continue to support industry share gains and margin expansion as end-market demand for industrial and Internet of Things compute needs begins to recover off current lows. Management has accelerated the drawdown of high customer inventory levels by shutting down manufacturing facilities, and current industry data as well as commentary from peers indicates that overall end demand is seeing early signs of improvement. The company has a demonstrated track record of margin expansion, and we expect to see gross margins trough at the current level and, through internal efficiencies and pricing initiatives for its Total System Solution, expand and drive increasing operating margins and higher levels of free cash flow.

Sells

Abbott Laboratories

We sold Abbott Laboratories given the full valuation and the complexity of its combined businesses. While we like the company’s continuous glucose monitoring business FreeStyle Libre and its aggregate medical device business, we are less excited about the prospects for its nutritional business and established pharmaceuticals business. Recent news of a large jury award at an infant formula competitor has us concerned that the overhang of this litigation could be an ongoing negative for Abbott for some time.

Accenture

We sold Accenture and see more limited upside for Accenture due to continuing trends of more selective IT budget spend and a reallocation of IT budgets to support AI initiatives. We believe growth rates for IT services will be lower over the next few years as enterprises continue to digest spending from the pandemic and focus on more cost-benefit analysis for IT initiatives, leading to longer sales cycles and more targeted projects.

Teleflex

We sold Teleflex given its below-peer revenue growth rates and seeming lack of participation in the broader pickup in health care utilization. Teleflex has struggled with recent acquisitions underperforming expectations, and the expected recovery in UroLift volumes remains elusive.

Outlook

The equity markets in the second quarter posted positive returns, led by the broadening secular trend in AI. The move in interest rates was muted in the quarter as markets await a clear signal from the Federal Reserve on the timing of a rate reduction. On the margin, economic activity slowed, with multiple ISM manufacturing readings in contraction territory and a weakening housing market. Equity valuations remain high, with AI-focused companies contributing the most to these elevated levels. The geopolitical situation remains very unsettled, and a U.S. presidential election moves into focus, adding to the level of uncertainty. With many issues unresolved, we could see markets move into a period of higher volatility off very low levels. The equity markets continue to reflect the positive backdrop of growing earnings and a potential lowering of interest rates. Our focus will continue to be at the company level, with an emphasis on seeking to invest in companies with secular tailwinds or strong product-driven cycles.

Disclosures

The opinions expressed herein are those of Aristotle Atlantic Partners, LLC (Aristotle Atlantic) and are subject to change without notice. Past performance is not a guarantee or indicator of future results. This material is not financial advice or an offer to purchase or sell any product. You should not assume that any of the securities transactions, sectors or holdings discussed in this report were or will be profitable, or that recommendations Aristotle Atlantic makes in the future will be profitable or equal the performance of the securities listed in this report. The portfolio characteristics shown relate to the Aristotle Atlantic Core Equity strategy. Not every client’s account will have these characteristics. Aristotle Atlantic reserves the right to modify its current investment strategies and techniques based on changing market dynamics or client needs. There is no assurance that any securities discussed herein will remain in an account’s portfolio at the time you receive this report or that securities sold have not been repurchased. The securities discussed may not represent an account’s entire portfolio and, in the aggregate, may represent only a small percentage of an account’s portfolio holdings. The performance attribution presented is of a representative account from Aristotle Atlantic’s Core Equity Composite. The representative account is a discretionary client account which was chosen to most closely reflect the investment style of the strategy. The criteria used for representative account selection is based on the account’s period of time under management and its similarity of holdings in relation to the strategy. Recommendations made in the last 12 months are available upon request.

Returns are presented gross and net of investment advisory fees and include the reinvestment of all income. Gross returns will be reduced by fees and other expenses that may be incurred in the management of the account. Net returns are presented net of actual investment advisory fees and after the deduction of all trading expenses.

All investments carry a certain degree of risk, including the possible loss of principal. Investments are also subject to political, market, currency and regulatory risks or economic developments. International investments involve special risks that may in particular cause a loss in principal, including currency fluctuation, lower liquidity, different accounting methods and economic and political systems, and higher transaction costs. These risks typically are greater in emerging markets. Securities of small‐ and medium‐sized companies tend to have a shorter history of operations, be more volatile and less liquid. Value stocks can perform differently from the market as a whole and other types of stocks.