Commentary

Global Equity 1Q 2023

(All MSCI index returns are shown net and in U.S. dollars unless otherwise noted.)

Markets Review

Sources: SS&C Advent, Bloomberg

Past performance is not indicative of future results. Aristotle Global Equity Composite returns are presented gross and net of investment advisory fees and include the reinvestment of all income. Gross returns will be reduced by fees and other expenses that may be incurred in the management of the account. Net returns are presented net of actual investment advisory fees and after the deduction of all trading expenses. Aristotle Capital Composite returns are preliminary pending final account reconciliation. Please see important disclosures at the end of this document.

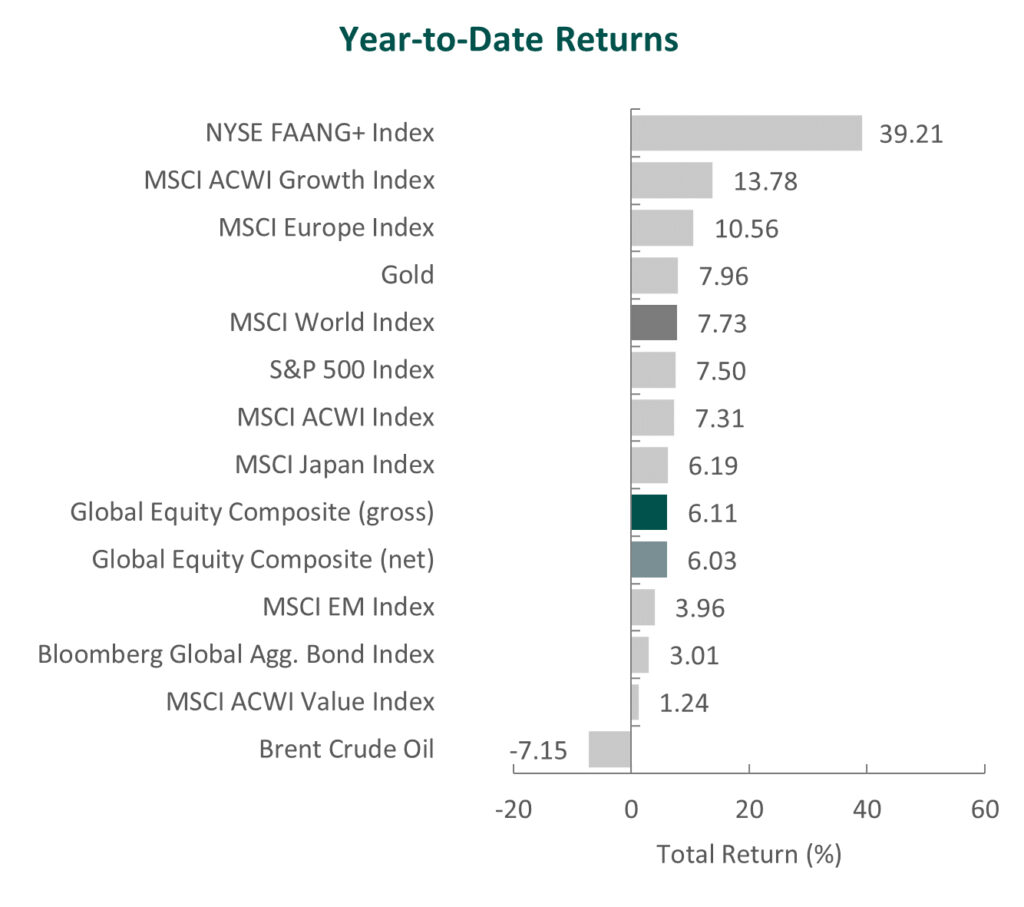

Global equity markets rose in the first quarter of the year, as the MSCI ACWI Index increased 7.31% during the period. Concurrently, the Bloomberg Global Aggregate Bond Index increased 3.01%. In terms of style, growth stocks outperformed their value counterparts during the quarter, with the MSCI ACWI Growth Index beating the MSCI ACWI Value Index by 12.54%.

Regionally, Latin America and Europe were the strongest performers during the quarter. On the other hand, Asia/Pacific ex-Japan and Emerging Markets were the weakest performers. On a sector basis, seven out of the eleven sectors within the MSCI ACWI Index posted gains, with Information Technology, Communication Services and Consumer Discretionary being the best performers. The worst performers were Energy, Health Care and Utilities.

Despite continued geopolitical tensions, persistent inflation and new concerns in the banking industry, the global economy proved to be resilient. This was seen by strong labor markets, robust household consumption and business investment in addition to effective management of Europe’s energy crisis. Additionally, China continued its relaxation of strict COVID rules by fully reopening its borders to travelers with all types of visas. As a result, the IMF increased its growth forecasts and now projects global growth of 3.4%, 2.9% and 3.1% in 2022, 2023 and 2024, respectively.

Inflation remained elevated in many regions, with the U.K, eurozone and U.S. reporting a 10.4%, 8.5% and 6.0% rate, respectively. Meanwhile, in Asia, Japan’s core consumer inflation hit a 41-year high of 4.2%. However, the pace of price increases moderated for other countries. This was the case for China and South Korea, where inflation rates declined to their lowest levels in 12 and 10 months, repectively. On a forward-looking basis, the IMF estimates global inflation will fall from 8.8% in 2022 to 6.6% in 2023 and 4.3% in 2024. The organization believes restrictive monetary policy and cooling commodity prices due to weaker demand will contribute to the pattern of disinflation.

During the quarter, the failure of U.S.-based, mid-sized institutions Silicon Valley Bank (SVB) and Signature Bank reverberated into the international market, adding a layer of complexity to restrictive central bank policies. After SVB’s closure due to a run on deposits, Credit Suisse also experienced withdrawals, further exacerbated by a subsequent plunging share price that led Swiss regulators to orchestrate a takeover by UBS. As a result of the turmoil in the banking sector, central banks in the U.S. and Europe have commented that credit conditions may have tightened more than some economic indicators currently suggest.

Lastly, on the geopolitical front, the war in Ukraine rages on in the eastern side of the country while southern lines have largely stabilized. Though China continues to align itself with Russia, China’s Ministry of Foreign Affairs released a paper calling for all parties to support dialogue to “gradually deescalate the situation.” Meanwhile, Western nations continue to support Ukraine, with commitments from the U.S., Germany and Britain to supply armored vehicles.

Performance and Attribution Summary

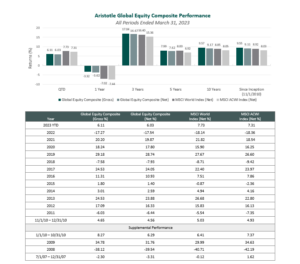

For the first quarter of 2023, Aristotle Capital’s Global Equity Composite posted a total return of 6.11% gross of fees (6.03% net of fees), underperforming the MSCI World Index, which returned 7.73%, and the MSCI ACWI Index, which returned 7.31%. Please refer to the table below for detailed performance.

| Performance (%) | 1Q23 | 1 Year | 3 Years | 5 Years | 10 Years | Since Inception* |

|---|---|---|---|---|---|---|

| Global Equity Composite (gross) | 6.11 | -3.32 | 17.04 | 7.99 | 9.57 | 9.55 |

| Global Equity Composite (net) | 6.03 | -3.62 | 16.67 | 7.62 | 9.17 | 9.11 |

| MSCI World Index (net) | 7.73 | -7.02 | 16.40 | 8.00 | 8.85 | 8.92 |

| MSCI ACWI Index (net) | 7.31 | -7.44 | 15.36 | 6.92 | 8.05 | 8.03 |

Source: FactSet

Past performance is not indicative of future results. Attribution results are based on sector returns which are gross of investment advisory fees. Attribution is based on performance that is gross of investment advisory fees and includes the reinvestment of income.

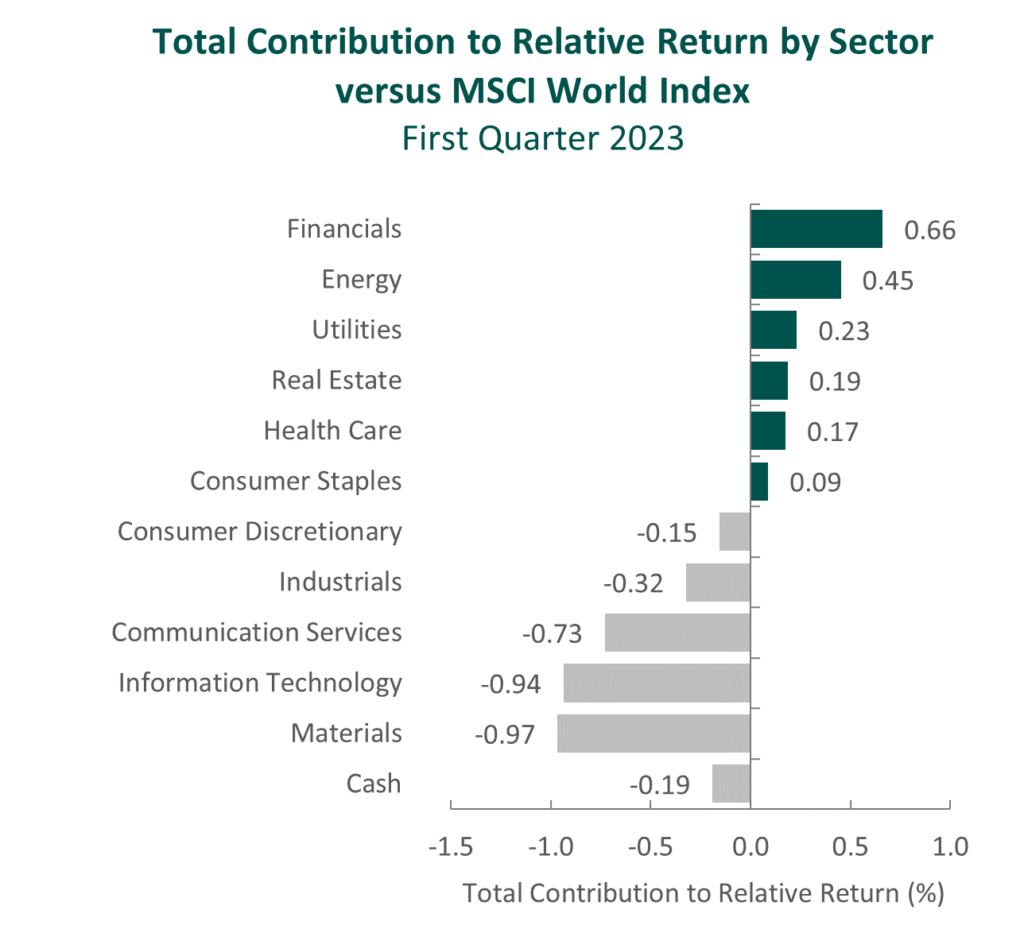

From a sector perspective, the portfolio’s underperformance relative to the MSCI World Index can be attributed to security selection, while allocation effects had a slightly positive impact. Security selection in Materials, Information Technology and Consumer Discretionary detracted the most from the portfolio’s relative performance. Conversely, security selection in Financials and Energy and an overweight in Consumer Discretionary contributed to relative return.

Regionally, both allocation effects and security selection were responsible for the portfolio’s underperformance relative to the MSCI World Index. Security selection in North America and Asia/Pacific ex-Japan detracted the most from relative performance, while an overweight in Europe and security selection in Japan contributed.

Contributors and Detractors for 1Q 2023

| Relative Contributors | Relative Detractors |

|---|---|

| Nemetschek | RPM International |

| Microchip Technology | Amgen |

| LVMH | Danaher |

| Lennar | Honeywell |

| Sony | General Dynamics |

RPM International, the coatings, sealants and building materials manufacturer, was one of the biggest detractors for the quarter. The combination of higher interest rates (which have negatively impacted construction activity and existing home sales), temporarily moderating customer purchases and cost inflation has weighed on the company and the overall coatings industry. Despite the challenging short-term macroeconomic landscape, RPM continues to demonstrate fundamental improvement. In response to inflation, the company has successfully increased pricing while simultaneously launching and executing on its latest Margin Achievement Plan (MAP 2025), which aims to make operational improvements by optimizing RPM’s manufacturing footprint, expanding categories of centralized procurement and executing on value-added selling. We believe the company’s ongoing focus on operational efficiency should allow it to continue to enhance its long-term FREE cash flow generation, which it can use to innovate new products and opportunistically deploy capital in the form of accretive acquisitions or returning value back to shareholders, as demonstrated by RPM’s ability to increase its dividend for 49 consecutive years.

Honeywell, the U.S.-based multinational industrial conglomerate, was one of the largest detractors during the quarter. Shares declined as management highlighted temporary issues affecting margins and the ability to meet demand in some of the company’s segments. These issues included component shortages in its Aerospace division, as well as severe cold weather that impacted production of its performance chemicals business. Despite the short-term setbacks, Honeywell continues to benefit from strong demand for its products across its various business segments. This is evidenced by the company’s record backlog, which grew to $29.6 billion in the fourth quarter—up 7% year-over-year. Additionally, during the quarter, CEO Darius Adamczyk announced he will step down in June of 2023 and hand the reins to current COO Vimal Kapur. Mr. Adamczyk built upon the work of his predecessor, famed former CEO David Cote, in the transformation of the business from what was once an over-leveraged, old-line industrial company to one poised for the digital age. We are impressed by Mr. Kapur’s 34-year tenure at Honeywell in increasingly important positions, including his leadership of Performance Materials and Technologies and Honeywell Building Technologies divisions. As such, we look forward to Mr. Kapur’s efforts to further advance Honeywell’s ability to leverage software across its massive industrial installed base and increase energy efficiency, productivity and connectivity (aka Industrial Internet of Things) for the company’s wide array of customers.

LVMH Moët Hennessy Louis Vuitton, the luxury goods company, was a primary contributor for the quarter. China, one of the world’s largest luxury goods markets, has reopened following three years of various COVID lockdown policies and provided a boost for LVMH. While we are pleased to see the company (and industry) benefit from an improved macroeconomic environment, this is not, and was not, our focus when analyzing the fundamentals of LVMH’s business. Instead of attempting to time short-term factors out of the company’s control, we remain fixated on what LVMH can control. This includes the company’s progress on initiatives such as integrating the acquisitions of Tiffany & Co. and, most recently, the Pedemonte Group to bolster its Jewelry division; market share gains within the Fashion & Leather Goods segment; continued market leadership with the likes of Dior’s Sauvage being named the world leader in perfumes for 2022; and the expansion of the company’s store network and the development of production facilities. These improvements, we believe, more directly impact the company’s long-term fundamental outlook, regardless of the short-term macroeconomic landscape. Lastly, LVMH appointed Pharrell Williams as its new Men’s Creative Director, filling the role following the tragic passing of Virgil Abloh in 2021.

Lennar, one of the nation’s largest homebuilders, was a primary contributor for the quarter. Following a housing surge supported by low mortgage rates and government stimulus, U.S. home sales activity began to decline in 2022 as rapidly rising mortgage rates reduced affordability. Over our decade-plus investment in Lennar, we have admired the management team’s ability to quickly respond to changing housing dynamics. Recent times were no exception, as Lennar adopted a dynamic pricing model that, in combination with its digital-marketing platform, helped to protect its backlog and prevent cancellations. As a result, fiscal first-quarter orders declined 10% year-over-year compared to a 38% decline for the homebuilder industry. The company has also made progress on its transition to a lighter asset strategy, a catalyst we previously identified, now controlling 68% of its land through options (up from 39% in 2020). Less capital tied up in land and the ability to acquire parcels on a just-in-time basis, in our opinion, should support enhanced FREE cash flow generation. As such, we believe Lennar’s strong balance sheet, prudent inventory management, and further ability to implement cost and production efficiencies position it well to both overcome near-term housing market softness and benefit from the decade-long undersupply of homes in the U.S.

Recent Portfolio Activity

| Buys | Sells |

|---|---|

| None | Brookfield Asset Management |

During the quarter, we sold our position in Brookfield Asset Management.

The strategy has been invested in Brookfield since the first quarter of 2022. In December 2022, the company completed the spinoff of 25% of its asset management business, now known as Brookfield Asset Management (“Manager,” ticker: BAM). As part of the spinoff, the parent company, Brookfield Corporation (“Corporation,” ticker: BN), retained a 75% interest in the Manager. As such, we decided to sell our stake in the Manager and use the proceeds to top-up our investment in the Corporation. While we continue to find the Manager’s business attractive, we view Brookfield Corporation as a more optimal investment.

Conclusion

A core tenet of our investment philosophy is the commitment to understand businesses with a long-term perspective. For us, this is especially important during times of heightened uncertainty when macroeconomic events dominate headlines. We remain aware of short-term topics such as inflation, monetary policy and the recent shock to the banking system. However, we believe a competitive advantage of our investment process lies in the fact that, instead of reacting and repositioning our portfolio based on unknowns and unfolding events, our focus remains on business fundamentals. Fundamentals, we are convinced, are what dictate shareholder value in the long term. As such, we continue to attentively study what we believe are high-quality companies with sustainable competitive advantages poised to outperform their peers over full market cycles.

The opinions expressed herein are those of Aristotle Capital Management, LLC (Aristotle Capital) and are subject to change without notice. Past performance is not a guarantee or indicator of future results. This material is not financial advice or an offer to buy or sell any product. You should not assume that any of the securities transactions, sectors or holdings discussed in this report were or will be profitable, or that recommendations Aristotle Capital makes in the future will be profitable or equal the performance of the securities listed in this report. The portfolio characteristics shown relate to the Aristotle Global Equity strategy. Not every client’s account will have these characteristics. Aristotle Capital reserves the right to modify its current investment strategies and techniques based on changing market dynamics or client needs. There is no assurance that any securities discussed herein will remain in an account’s portfolio at the time you receive this report or that securities sold have not been repurchased. The securities discussed may not represent an account’s entire portfolio and, in the aggregate, may represent only a small percentage of an account’s portfolio holdings. The performance attribution presented is of a representative account from Aristotle Capital’s Global Equity Composite. The representative account is a discretionary client account which was chosen to most closely reflect the investment style of the strategy. The criteria used for representative account selection is based on the account’s period of time under management and its similarity of holdings in relation to the strategy. Recommendations made in the last 12 months are available upon request.

Returns are presented gross and net of investment advisory fees and include the reinvestment of all income. Gross returns will be reduced by fees and other expenses that may be incurred in the management of the account. Net returns are presented net of actual investment advisory fees and after the deduction of all trading expenses.

All investments carry a certain degree of risk, including the possible loss of principal. Investments are also subject to political, market, currency and regulatory risks or economic developments. International investments involve special risks that may in particular cause a loss in principal, including currency fluctuation, lower liquidity, different accounting methods and economic and political systems, and higher transaction costs. These risks typically are greater in emerging markets. Securities of small‐ and medium‐sized companies tend to have a shorter history of operations, be more volatile and less liquid. Value stocks can perform differently from the market as a whole and other types of stocks.

The material is provided for informational and/or educational purposes only and is not intended to be and should not be construed as investment, legal or tax advice and/or a legal opinion. Investors should consult their financial and tax adviser before making investments. The opinions referenced are as of the date of publication, may be modified due to changes in the market or economic conditions, and may not necessarily come to pass. Information and data presented has been developed internally and/or obtained from sources believed to be reliable. Aristotle Capital does not guarantee the accuracy, adequacy or completeness of such information.

Aristotle Capital Management, LLC is an independent investment adviser registered under the Investment Advisers Act of 1940, as amended. Registration does not imply a certain level of skill or training. More information about Aristotle Capital, including our investment strategies, fees and objectives, can be found in our Form ADV Part 2, which is available upon request. ACM-2304-95

Composite returns for all periods ended March 31, 2023 are preliminary pending final account reconciliation.

The Aristotle Global Equity Composite has an inception date of November 1, 2010; however, the strategy initially began at Howard Gleicher’s predecessor firm in July 2007. A supplemental performance track record from January 1, 2008 through October 31, 2010 is provided on this page and complements the Global Equity Composite presentation that is located at the end of this presentation. The performance results were achieved while Mr. Gleicher managed the strategy at a prior firm. The returns are those of a publicly available mutual fund from the fund’s inception through Mr. Gleicher’s departure from the firm. During that time, Mr. Gleicher had primary responsibility for managing the fund.

Past performance is not indicative of future results. The information provided should not be considered financial advice or a recommendation to purchase or sell any particular security or product. Performance results for periods greater than one year have been annualized.

Returns are presented gross and net of investment advisory fees and include the reinvestment of all income. Gross returns will be reduced by fees and other expenses that may be incurred in the management of the account. Net returns are presented net of actual investment advisory fees and after the deduction of all trading expenses.

The MSCI World Index is a free float-adjusted market capitalization weighted index that is designed to measure the equity market performance of developed markets. The MSCI World Index consists of the following 23 developed market country indices: Australia, Austria, Belgium, Canada, Denmark, Finland, France, Germany, Hong Kong, Ireland, Israel, Italy, Japan, Netherlands, New Zealand, Norway, Portugal, Singapore, Spain, Sweden, Switzerland, the United Kingdom and the United States. The MSCI Emerging Markets Index is a free float-adjusted market capitalization-weighted index that is designed to measure equity market performance of emerging markets. The MSCI Emerging Markets Index consists of the following 24 emerging market country indexes: Brazil, Chile, China, Colombia, Czech Republic, Egypt, Greece, Hungary, India, Indonesia, Korea, Kuwait, Malaysia, Mexico, Peru, Philippines, Poland, Qatar, Saudi Arabia, South Africa, Taiwan, Thailand, Turkey and United Arab Emirates. The MSCI ACWI captures large and mid-cap representation across 23 developed markets and 24 emerging markets countries. With approximately 3,000 constituents, the Index covers approximately 85% of the global investable equity opportunity set. The MSCI ACWI Growth Index captures large and mid-cap securities exhibiting overall growth style characteristics across 23 developed markets countries and 24 emerging markets countries. The MSCI ACWI Value Index captures large and mid-cap securities exhibiting overall value style characteristics across 23 developed markets countries and 24 emerging markets countries. The MSCI Europe Index captures large and mid-cap representation across 15 developed markets countries in Europe. With more than 400 constituents, the Index covers approximately 85% of the free float-adjusted market capitalization across the European developed markets equity universe. The MSCI Japan Index is designed to measure the performance of the large and mid-cap segments of the Japanese market. With approximately 250 constituents, the Index covers approximately 85% of the free float-adjusted market capitalization in Japan. The S&P 500® Index is the Standard & Poor’s Composite Index of 500 stocks and is a widely recognized, unmanaged index of common stock prices. The NYSE FAANG+ Index is an equal-dollar-weighted index designed to represent a segment of the Information Technology and Consumer Discretionary sectors consisting of highly traded growth stocks of technology and tech-enabled companies, such as Facebook, Apple, Amazon, Netflix and Alphabet’s Google. The Bloomberg Global Aggregate Bond Index is a flagship measure of global investment grade debt from 28 local currency markets. This multi-currency benchmark includes Treasury, government-related, corporate and securitized fixed rate bonds from both developed and emerging markets issuers. The Brent Crude Oil Index is a major trading classification of sweet light crude oil that serves as a major benchmark price for purchases of oil worldwide. The volatility (beta) of the Composite may be greater or less than the benchmarks. It is not possible to invest directly in these indices.